NRE deposits are deposits made by NRIs in Indian Rupees. The interest earned is completely tax-free. NRE deposit is akin to an investor converting foreign currency, most notably USD, into Indian Rupees (INR) and then making a Fixed deposit in INR. Such deposits help in creating demand for INR, thereby stemming the depreciation of INR, or an appreciation of INR vis a vis the foreign currency.

For the investor, the returns need to be calculated after factoring in the change in the exchange rate. For example, let us say the current USD/INR exchange rate is 80 (80 INR to 1 USD). A Non-Resident converts USD10,000 into INR @Rs.80, which works out to Rs. 800,000. Assuming that the NRE deposit earns interest @5%, this amount grows to Rs.840,000. Meanwhile, in 1 year, the INR has depreciated to say 82.

Thus, Rs.840,000 is now equal to USD 10,244. In other words, the NRI investor earns a return of 2.44% in USD terms. This is advantageous to him/her if, during the period when the NRE deposit was made, the interest rate on 1 year USD deposit rate is less than 2.44%. However, if the interest rates on deposits in USD are higher than 2.44%, then the NRI investor is better off making deposits in USD, rather than in INR.

The RBI uses the interest rate on NRE deposits as a tool to manage/influence the USD/ INR exchange rate. The higher the rate, the greater the incentive for NRIs to opt for NRE deposits. If this flow is large enough, the INR may not slide to 82. Another incentive is that the interest earned on NRE deposits is completely tax-free. This adds to the interest rate differential between USD and NRE deposit rates.

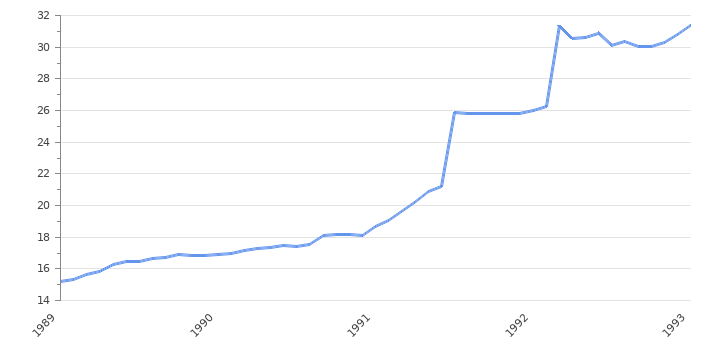

In an extremely competitive global market, the RBI has been skewed towards having a competitive exchange rate. As can be seen from the graph below, the Rupee is seen sliding slowly and in the event of a sudden, sharp depreciation, it remains stable for a relatively long period.

Keeping the interest rates on NRE deposits low stems from the flow of foreign currency into India, and to that extent, helps in stabilizing an appreciating INR. However, in the event of a sudden sharp depreciation of INR, increasing rates help in increasing the inflow of foreign currency and stabilizes the currency.

FCNRB deposits are deposits made in Foreign Currency by Non-Residents with Indian Banks. In the case of FCNR, there is no conversion of foreign currency into INR and hence, there is no associated exchange rate risk. FCNR deposits compete directly with other Investments in Foreign Currency. An increase in FCNR deposits increases the Reserves of the economy. Thus, the country is in a better position to tap reserves and support the INR in the event of sharp depreciation. RBI has indulged in providing measured support to INR against the USD by selling USD and buying INR.

Stay updated with the latest market and investment updates. Join Jama Wealth on Telegram, Linkedin, YouTube, Instagram, Facebook, Quora for more!

For high quality investment advice and to grow wealth, download Jama Wealth App on iOS App Store and Android Play Store.