Imagine a cricket match where the final overs are as crucial as the opening ones. Retirement planning in India is like that decisive part of the game. You’ve played well all your life, and now it’s time to ensure a winning finish. With life expectancy rising and the concept of joint family support waning, retirement planning has become more critical than ever in India.

The retirement landscape in India is shifting dramatically. Gone are the days when retirement meant a quiet life with limited needs. Today’s retirees dream of a vibrant post-work life, filled with travel, hobbies, and active social engagement. However, this dream can only be realised through meticulous planning and disciplined investment. As a SEBI Registered Investment Advisor, I see retirement planning as an essential journey, not just a destination. It’s about ensuring that your golden years are truly golden, financially secure, and fulfilling.

Concept of Retirement Planning in India

Retirement planning in India is a dynamic process that goes far beyond mere accumulation of wealth. It’s similar to preparing for a grand festival – requiring anticipation, detailed planning, and adequate resources. Without a solid plan, just as a festival loses its sheen, retirement years may lack the lustre they deserve.

The Essence of Retirement Planning

The primary goal of retirement planning is to ensure that the post-retirement phase is as fulfilling as the working years. It’s about scripting a second act that’s rich in experiences and devoid of financial worries. This phase should be envisioned as an extended celebration of life, where financial stability allows one to pursue long-held passions or simply enjoy a life of leisure and tranquillity. There is a new trend of Financial Independence & Early Retirement Planning (FIRE), where people would love to go beyond their usual retirement and do something meaningful in their lives.

Retirement isn’t an end, but a beginning of a new chapter that can be as exciting as one’s youth. Whether it’s peaceful solitude in the hills or an adventurous, globe-trotting lifestyle, retirement plans must be robust enough to support these dreams. A strong financial foundation is critical, similar to the foundation of a house, providing strength and stability while being flexible enough to adapt to changing needs.

The Dual Phases of Retirement Planning

Accumulation Phase – Building the Corpus

This phase is all about saving and investing wisely. The focus here is to build a substantial retirement corpus through various investment vehicles. Understanding and leveraging retirement pension plans in India, such as the EPF, PPF, and NPS, plays a crucial role. This phase is about growth and accumulation, where one’s savings are directed towards building a nest egg for the future.

Decumulation Phase – Managing the Wealth

As important as accumulation, the decumulation phase involves planning how to utilise the accumulated wealth. It’s about ensuring a steady income stream post-retirement and involves making decisions about how and when to withdraw from savings. This phase requires careful planning to ensure that the retirement corpus lasts throughout the retirement years, factoring in inflation, healthcare costs, and other unforeseen expenses.

Planning Decade Wise

Strategizing Investments Over Time:

Effective retirement planning involves strategizing investments over different decades of one’s life. In the initial years, one might adopt a more aggressive investment approach, gradually moving towards more conservative investments as retirement nears. This shift is crucial to protect the accumulated corpus from market volatilities and to ensure its availability during retirement years.

Adjusting Plans as Per Changing Needs:

Just as life evolves, so should the retirement plan. It’s vital to reassess and readjust the retirement strategy in response to life’s milestones and changing financial landscapes. This adaptability is key to maintaining a retirement plan that stays aligned with personal goals and external economic conditions.

Comprehensive Steps in Retirement Planning

Retirement planning in India is a meticulous process, similar to crafting a masterful piece of art. Each stroke, each colour choice matters, just like every decision in the journey of retirement planning shapes the final picture of your golden years.

1. Assessing Current Financial Situation

Understanding Your Financial Health

The first step in retirement planning is similar to a cricket team analysing its performance before a big match. Assess your current income sources and monthly expenses. This step is fundamental, as it sets the stage for all subsequent planning. Consider your regular income, any side income sources, and your monthly expenses. This assessment gives a clear view of your financial health and how much you can allocate towards retirement savings.

Assets and Liabilities Evaluation

Next comes a thorough evaluation of what you own and owe. List down all your assets, including savings, investments, real estate, and any other valuables. Then, subtract your liabilities like loans and debts. This calculation of your net worth is a vital indicator of your financial stability and a guiding light for your retirement planning journey.

2. Setting Retirement Goals

Envisioning Your Retirement

Imagine your ideal retirement – is it a quiet life in the lap of nature, or a bustling social life in the city? Setting clear lifestyle goals for retirement is crucial. It helps in creating a roadmap to achieve them. This process is not just about financial planning but aligning your retirement vision with your personal aspirations.

Planning for Health and Leisure

A critical, yet often overlooked aspect of retirement planning, is preparing for healthcare and leisure costs. Healthcare expenses tend to increase with age, and planning for these costs is essential for a stress-free retirement. Also, consider budgeting for hobbies and leisure activities, which add joy and fulfilment to your retirement years.

3. Estimating Retirement Corpus in India: A Guide To Various Approaches

Accurately estimating the retirement corpus requires a thorough understanding of one’s current financial situation, future needs, and the unpredictability of external factors like inflation and market dynamics. This guide delves into various methodologies, from simple rule-of-thumb calculations to more complex simulations, to help you chart your retirement journey with greater confidence.

Simple Methods for Corpus Estimation

Rule of Thumb: The 25 Times Rule

A widely used starting point is to multiply your annual expenses by 25. For instance, if your annual expenses are INR 6 lakhs, your estimated retirement corpus should be around INR 1.5 crores. This method assumes a 4% withdrawal rate mentioned above, considered a safe standard globally.

Given India’s higher inflation rates, it’s prudent to revise this multiple to at least 30 times your annual expenses. This adjustment helps in creating a buffer against inflation and other unforeseen expenses in retirement.

Example 1: Mr. Gupta

Situation: Mr. Gupta, aged 45, plans to retire at 60 and expects to live till 85. His current annual expenses are INR 8 lakhs.

Estimation Using Rule of Thumb: By the 25 times rule, his corpus requirement would be INR 2.0 crores. However, considering inflation and lifestyle changes, a safer estimate might be closer to INR 2.5 crores.

Number of Years to Retirement Approach

This method involves multiplying your current annual expenses by the number of years you expect to live post-retirement. For instance, if you spend INR 6 lakhs annually and expect to live 25 years post-retirement, your estimated corpus would be INR 1.5 crores.

It’s crucial to factor in inflation and possible changes in lifestyle. Your expenses in retirement might differ significantly from your current spending patterns, necessitating a more personalised estimate.

More Complex Methods for Accurate Estimation

Human Life Value (HLV) Method

The Human Life Value (HLV) method offers a personalised approach to estimating your required retirement corpus. This method intricately calculates the present value of future earnings and deducts any existing liabilities, thereby painting a realistic picture of one’s financial future.

Imagine your annual income stands at INR 10 lakhs, and you foresee a career span of another 20 years. Simple arithmetic suggests your total earnings would amount to INR 2 crores. However, the HLV method takes this a step further by factoring in the critical element of inflation, which affects the future value of money. After adjusting for inflation, which diminishes the value of future earnings, and subtracting your current liabilities, the resulting figure represents a more accurate estimate of the corpus you would need to accumulate for a comfortable retirement.

This method’s significance lies in its consideration of individual-specific factors. It doesn’t just look at your current earnings but also contemplates your career growth trajectory, potential income increases, and any foreseeable financial obligations. By providing a tailored estimate, the HLV method in retirement planning serves not just as a calculator but as a personalised financial roadmap.

Example 2: Ms. Ghosh

Situation: Ms. Ghosh, aged 35, earns INR 12 lakhs per annum and expects significant career growth. She has a current corpus of INR 30 lakhs and plans to retire at 55.

Using the HLV method and factoring in her career growth, her corpus requirement might be upwards of INR 5 crores. Monte Carlo simulations (explained below) can further refine this estimate by considering various market and inflation scenarios.

Monte Carlo Simulations

Monte Carlo simulations involve running numerous scenarios with different variables like life expectancy, inflation rates, and investment returns. This method provides a range of possible outcomes for your retirement corpus, helping you prepare for various contingencies.

Assume you have a current corpus of INR 50 lakhs, and you contribute INR 1 lakh annually towards retirement. By running simulations with different rates of return and inflation scenarios, you can estimate the probability of your corpus lasting through your retirement years.

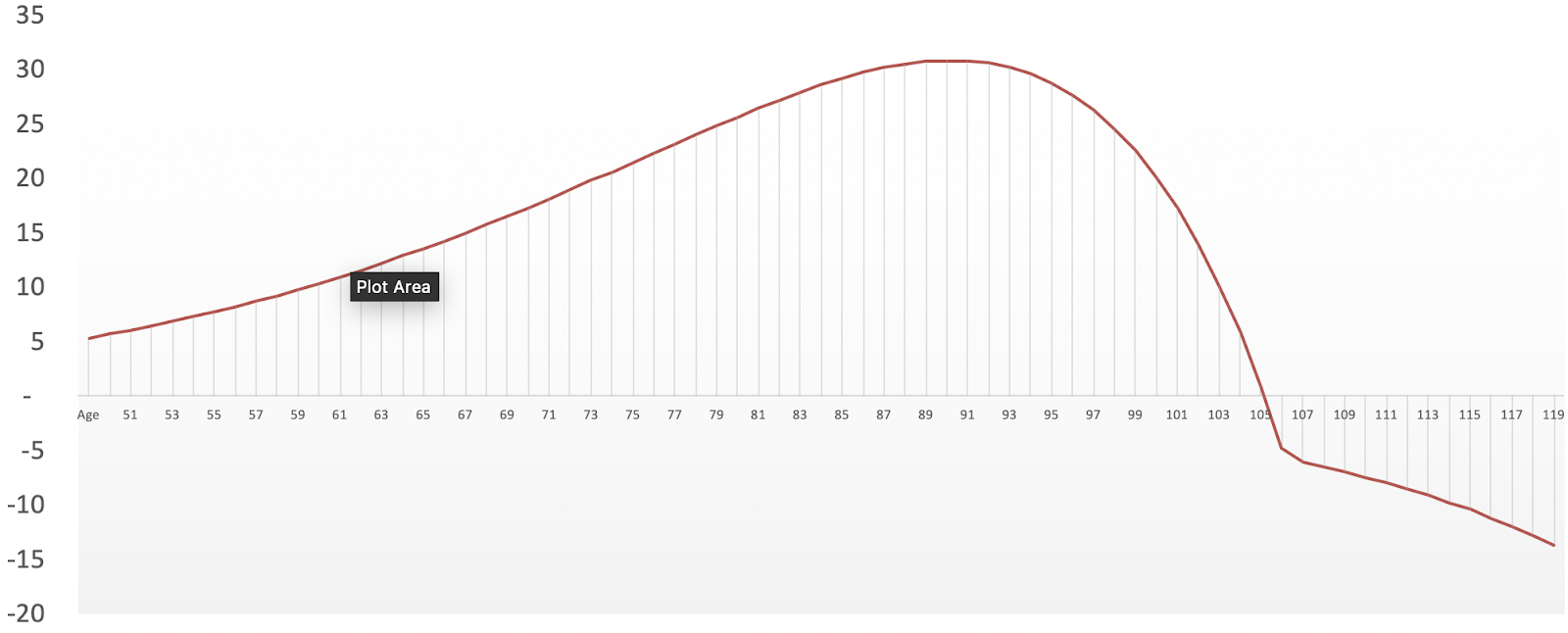

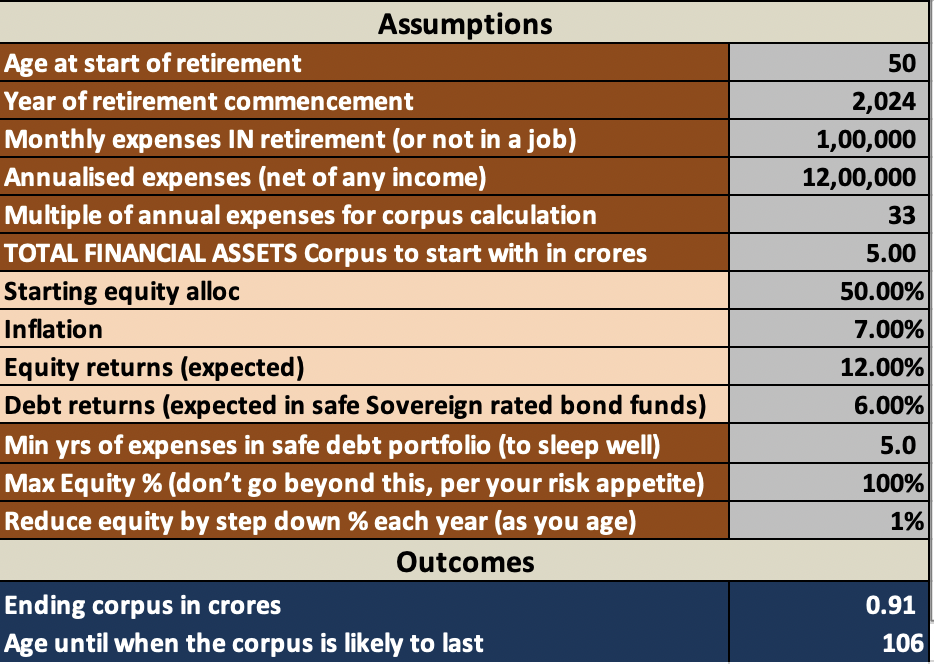

The following is an illustration of how a retirement corpus can compound further over time and then decumulate as well. In the case below, the corpus will run out at age 106 which is well beyond the life expectancy of a healthy female in India which is around 80 years. The complete list of assumptions is attached below. One can run multiple simulations to see which set of assumptions is closest to one’s personal situation.

Estimating the retirement corpus in India is a nuanced process that requires a blend of simple rule-of-thumb methods and more sophisticated approaches like the HLV method and Monte Carlo simulations. The key is to start with a basic estimate and refine it over time, considering personal career trajectories, lifestyle aspirations, and external economic factors.

3. Choosing Asset Allocation & Investment Philosophy for Retirement Plan

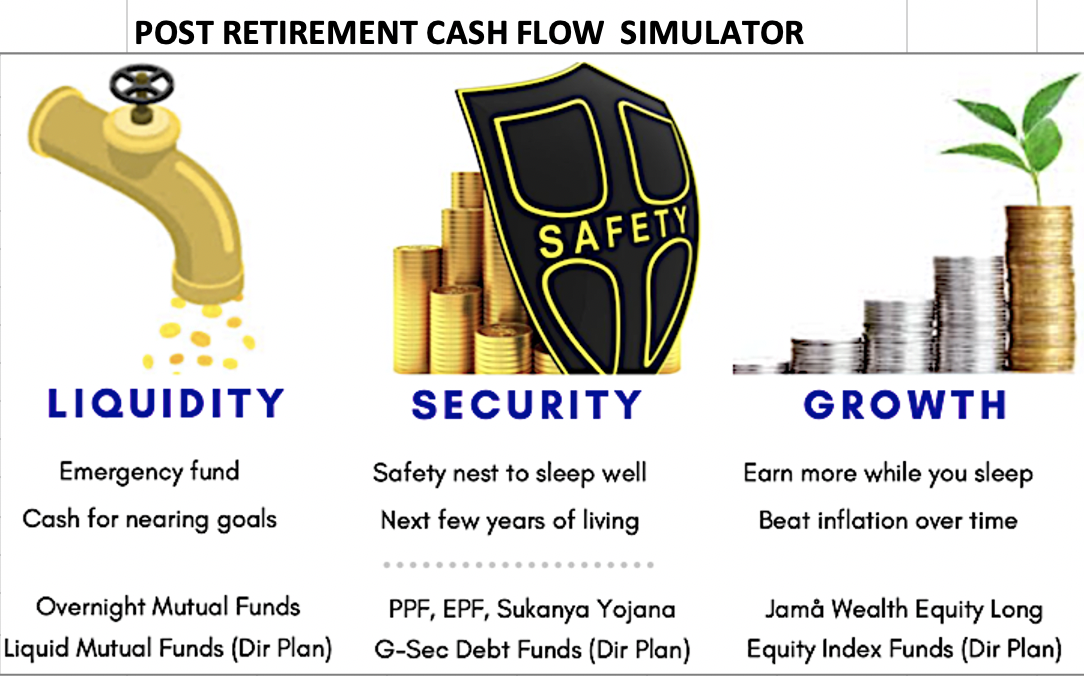

In the context of retirement planning in India, the LSG (Liquidity, Safety, Growth) framework, advocated by Jama Wealth, emerges as a comprehensive strategy. This approach is instrumental in sculpting a retirement plan that’s not only robust but also well-aligned with an individual’s financial goals and risk profile.

The LSG Framework

Liquidity

The first pillar, Liquidity, ensures that your portfolio has sufficient liquid assets to meet immediate and short-term needs. This is crucial during retirement when regular income streams might diminish. Maintaining a portion of your investments in liquid assets like short-term debt funds or liquid mutual funds, as advised by Jama Wealth, can provide the necessary financial flexibility and quick access to funds in emergencies or for regular expenses.

Safety

Safety, the second aspect, is about protecting the capital. In retirement planning, preserving the hard-earned corpus is as crucial as growing it. Here, a well-structured debt portfolio, curated with expert advice from Jama Wealth, plays a key role. By investing in high-quality debt instruments and mutual funds, retirees can safeguard their principal amount while receiving steady, albeit lower, returns. One can consider this as an amount to ‘sleep well’ at night; often translating to 5 or 7 years of funded expenses.

Growth

Lastly, Growth focuses on long-term wealth creation, essential for beating inflation and maintaining lifestyle standards in retirement. Jama Wealth’s Portfolio Management Services (PMS) in the ‘Jewel’ and ‘Spark’ strategies adeptly incorporate equities into the retirement portfolio. Equities, despite their volatility, are pivotal for achieving higher returns over the long term. These strategies, under the aegis of Jama Wealth, are designed to optimise growth potential while managing risk, making them an integral component of a well-rounded retirement plan.

In essence, the LSG framework with Jama Wealth’s strategic guidance provides a holistic approach to retirement planning in India. It balances immediate financial needs with long-term growth aspirations, ensuring a secure and prosperous retirement phase.

The Roots & Wings Investment Philosophy

In the ever-evolving landscape of retirement planning in India, the Roots and Wings investment philosophy, as advocated by Jama Wealth, stands out as a pivotal strategy, especially when addressing the challenges posed by inflation. This philosophy, adeptly crafted for the growth and protection of retirement corpus, strikes a fine balance between stability and growth, aligning seamlessly with the objectives of a robust retirement plan.

Roots

The Foundation of Stability: In this approach, ‘Roots’ symbolises investments in companies with strong foundational elements. These are firms characterised by solid balance sheets, low debt, high return on equity, and exemplary management. Such investments act as the bedrock of your portfolio, providing stability and safety. They are similar to the deep roots of a tree, offering sustenance and resilience amidst economic fluctuations. In the context of retirement planning, these ‘Roots’ investments are crucial as they offer protection against market volatility, thereby safeguarding the corpus from significant downturns.

Wings

Pursuing Growth to Counter Inflation: On the flip side, ‘Wings’ represents investments in high-growth companies. These are typically market leaders or emerging players with potential for consistent revenue and profit growth. In retirement planning, the ‘Wings’ component is critical to combat the eroding effects of inflation. While debt instruments offer safety, they often fall short in outpacing inflation over the long term. Equities, represented by ‘Wings’, fill this gap by offering the potential for higher returns, thus ensuring that your retirement corpus not only remains protected but also grows in real terms.

Jama Wealth’s implementation of this investment philosophy in retirement planning is both strategic and nuanced. By integrating ‘Roots’ and ‘Wings’, they create a diversified portfolio that aims for stability while capturing growth opportunities. This approach is particularly effective for retirees who need to balance the immediacy of stable returns with the long-term necessity of inflation-beating growth.

In summary, the Roots and Wings investment philosophy offers a comprehensive solution for retirees. It smartly addresses the dual need for protecting the retirement corpus against market vagaries while ensuring its real growth over time. For anyone navigating the complexities of retirement planning in India, this philosophy, as leveraged by Jama Wealth, provides a well-rounded approach to achieving financial serenity in their golden years.

4. Choosing the Right Retirement Plan

India’s retirement planning landscape offers a variety of pension plans, each tailored for different needs. From traditional government retirement plans in India like the EPF and PPF to more modern options like mutual fund-linked retirement plans, the choices are abundant. Each plan’s unique features, such as the risk profile, return potential, and tax benefits, need careful consideration.

Don’t just glance at the potential returns; get into the details of each plan. Compare the benefits, features, liquidity options, and tax implications. This detailed analysis is crucial in choosing a retirement plan that best aligns with your retirement goals and risk appetite. In the subsequent section we will cover various government retirement plans and compare them with private plans.

5. Creating a Retirement Budget

A significant step in retirement planning is estimating your expenses during retirement. While we have covered the estimation in great detail in Step 2 above and also in the Safe Withdrawal Rule (covered below), we are still reiterating it as a step here.

Do not forget inflation which will likely impact future costs, so factor this into your calculations. This foresight helps in determining how much you need to save today to enjoy your desired lifestyle tomorrow.

Allocate your resources between necessities and luxuries. This allocation should be thoughtful, considering your post-retirement needs and aspirations. It’s about creating a balance, ensuring you have enough for the essentials while also setting aside funds for enjoyment and leisure.

6. Regularly Reviewing and Adjusting

Staying Aligned with Life’s Changes: Your retirement plan should be as dynamic as life itself. Regularly review your plan to ensure it stays on track with any significant life changes, such as a change in income, marital status, or health. This adaptability is key to maintaining a relevant and effective retirement plan.

Economic fluctuations can impact your investments and savings. Therefore, be prepared to adjust your retirement plan in response to market conditions. This responsiveness is crucial in mitigating risks and ensuring your retirement savings grow steadily.

The above five steps are part of a multi-faceted process that involves a thorough assessment of your current financial situation, setting clear retirement goals, choosing the right retirement plan, creating a budget, and regular reviews and adjustments. This process is not just about accumulating wealth; it’s about strategically planning for a future where financial security and personal fulfilment coexist harmoniously.

Understanding the 4% Safe Withdrawal Principle in Indian Retirement Planning

Now that we have laid out all the key concepts in retirement planning, let us examine how it goes beyond just accumulating a significant corpus. It also involves strategizing how to withdraw these savings post-retirement. Another critical concept in this phase is the ‘Safe Withdrawal Rate’ (SWR), a rule of thumb aimed at ensuring that one’s retirement savings last throughout their post-retirement years. In global financial planning, the 4% rule is a commonly discussed SWR, and its application in the Indian context is worth exploring.

The Essence of the 4% Rule

Originating from the Trinity Study, the 4% rule suggests that retirees can withdraw 4% of their retirement corpus in the first year of retirement, adjusting the amount each subsequent year for inflation. The principle behind this rule is to provide a steady income stream while preserving the principal over a 30-year retirement period.

When applying this rule to retirement planning in India, it’s crucial to consider factors like inflation rates, which tend to be higher than in western countries, and the longevity of retirees. Therefore, a conservative approach may involve adjusting the withdrawal rate to a lower percentage.

Integrating the 4% Rule in Indian Retirement Plans

Each individual’s retirement plan is unique, with differing lifestyle requirements, health expenses, and other variables. While the 4% rule offers a starting point, it must be tailored to the specific needs and circumstances of Indian retirees, considering factors such as existing retirement pension plans in India and other income sources.

The key challenge in retirement planning is to strike a balance between having enough to spend each year and ensuring that the corpus does not deplete prematurely. This balance is critical in the Indian context, where joint family systems and intergenerational support might also play a role in retirement planning.

Considerations Beyond the 4% Rule

Tailoring this rule to fit the Indian retirement landscape, along with regular monitoring and adjustments, is key to ensuring a secure and comfortable retirement. Here are some considerations:

- Inflation significantly impacts the value of money and purchasing power over time. In India, with its historically higher inflation rates, the 4% rule must be adapted to ensure that withdrawals keep pace with inflation without exhausting the retirement fund too quickly.

- The investment strategy during the decumulation phase is just as crucial as during the accumulation phase. The choice of assets – whether in equity, debt, or other instruments – should be aligned with the SWR to ensure that the portfolio can support the withdrawals while mitigating risks.

- The retirement planning process including withdrawal strategies, should be dynamic. Regular reviews and adjustments are essential to account for changes in market conditions, personal health status, and other unforeseen life events.

- While the 4% rule is a valuable guideline in retirement planning, its application in India requires careful consideration of local economic conditions, individual lifestyle choices, and financial goals. Aspects like inflation, life expectancy, and investment strategy play a significant role in determining the appropriate withdrawal rate.

Retirement planning in India is about tweaking these parameters and arriving at a balance between saving enough to secure a comfortable retirement while also investing smartly to ensure that the retirement corpus grows and lasts throughout the retirement years. With thoughtful planning, disciplined saving, and prudent investing, one can ensure that their retirement years are not just secure, but also immensely fulfilling.

Top Retirement Plans in India: A Comprehensive Overview

Retirement plans in India are as diverse and colourful as our country itself. From the sturdy EPF to the adaptable NPS, and from market-linked plans to traditional pension policies, each plan offers unique advantages and caters to different retirement needs. Choosing the right retirement plan is a personal journey that should align with your individual retirement goals, risk appetite, and long-term aspirations. With the right plan, your retirement can be a time of joy, fulfilment, and financial security, much like a well-planned festival that brings happiness and celebration to life.

Various Retirement Plan Options in India

The Dependable EPF: The Employees’ Provident Fund (EPF) stands as a towering banyan tree in India’s retirement planning garden – grand, dependable, and deeply rooted. It’s a government-backed scheme that guarantees returns, making it a preferred choice for those seeking stability and reliability in their retirement corpus.

The Versatile NPS: On the other hand, the National Pension System (NPS) is like a versatile river, meandering through varied investment landscapes. It offers a mix of equity, corporate bonds, and government securities, making it suitable for individuals with varying risk appetites. The NPS is flexible, allowing one to choose between different asset classes and change their investment choices over time.

Mutual Fund-Linked Retirement Plans: These plans are like the monsoon winds – dynamic and capable of bringing significant gains. They offer market-linked returns, which can be higher than traditional fixed-return investments. Suitable for those who have a good understanding of market dynamics and are willing to take on higher risk for potentially greater rewards.

Traditional Pension Policies: Offered by insurance companies, these are similar to a well-manicured garden – offering predictability and stability. These policies typically provide fixed returns and are suitable for individuals who prefer a conservative approach to retirement planning.

Tailoring Retirement Plans to Your Individual Needs

Just as India’s diverse cuisine caters to different palates, retirement plans in India offer a range of investment options to suit different tastes and retirement goals. From aggressive equity-oriented plans for the risk-takers to conservative debt plans for the risk-averse, there’s something for everyone.

Some plans allow customization, enabling investors to tweak their investment portfolios as per their life stage and changing financial goals. This flexibility is crucial in a country as diverse as India, where retirement needs and expectations vary greatly from person to person.

Comparing Retirement Plan Features

Here is a quick checklist on how to compare various retirement plan features.

- When comparing retirement plans, it’s important to assess each plan’s risk and return profile. This is similar to choosing the right ingredients for a balanced meal – each component should complement the other, ensuring a healthy and satisfying diet.

- Another key aspect is understanding the tax implications of each retirement plan. Just like navigating through India’s intricate tax laws, understanding the tax benefits and liabilities of each plan is crucial for effective retirement planning.

- Aligning with Retirement Visions: Each retirement plan should align with your long-term retirement vision. Whether it’s travelling across India in your golden years or enjoying a peaceful life surrounded by loved ones, your chosen retirement plan should support these dreams.

- Evaluating Liquidity and Flexibility: It’s also essential to consider the liquidity and flexibility of retirement plans. Plans with higher liquidity are like having a backup generator; they provide financial support in case of unexpected emergencies.

Case Studies in Retirement Planning

Real-life success stories help show the way to implement the points discussed above. These stories serve as practical examples, highlighting the effectiveness of different strategies and choices in retirement planning.

Case Study 1: The Saga of Mr. Sharma: A Government Employee’s Journey

Mr. Sharma’s story is similar to a well-played, disciplined innings in a cricket match. Throughout his career as a government employee, he consistently invested in the Employees’ Provident Fund (EPF) and the Public Provident Fund (PPF). These traditional government retirement plans in India are known for their safety and steady returns.

By the time of his retirement, Mr. Sharma had accumulated a substantial corpus. His investment in these good retirement plans in India paid off, providing him with a secure and comfortable retirement. His journey exemplifies the power of consistency and the importance of starting early in the world of retirement planning.

Case Study 2: Mrs. Iyer’s Tale: Embracing Diversification

In contrast to Mr. Sharma, Mrs. Iyer’s approach was more diversified. She chose a mix of the National Pension System (NPS) and mutual funds for her retirement planning. This strategy aligned well with her higher risk appetite and desire for potentially greater returns.

Mrs. Iyer’s story is a testament to the effectiveness of strategic planning and diversification in retirement planning schemes in India. Her investments not only grew over time, but she also had a diversified portfolio that minimised risks and maximised returns, showcasing the benefits of blending different types of retirement plans.

Comparing the journeys of Mr Sharma and Mrs Iyer

These two contracting journeys have several points worth highlighting.

- The Importance of Early Planning

Both Mr. Sharma and Mrs. Iyer began their retirement planning early in their careers. Starting early gives your investments more time to grow, benefitting from the power of compounding. It’s a crucial lesson for anyone looking to ensure financial security in their retirement years.

- Diversification as a Key Strategy

Mrs. Iyer’s approach demonstrates the importance of diversification. By spreading her investments across different asset classes, she was able to balance risk and maximise returns. This strategy is especially relevant in the volatile economic environment of India, where market dynamics can significantly impact investment outcomes.

- Choosing the Right Retirement Plans

Selecting the right retirement plans is crucial. While Mr. Sharma preferred the safety of government retirement plans in India, Mrs. Iyer was inclined towards plans offering market-linked returns. Their choices were aligned with their individual risk appetites and retirement goals, emphasising the need to tailor retirement planning to personal financial situations.

- Regular Reviews and Adjustments

Both individuals periodically reviewed and adjusted their investment portfolios in response to changing market conditions and personal circumstances. This adaptability is key in ensuring that retirement plans remain effective and relevant over the long term.

These real-life stories highlight several key aspects of successful retirement planning in India. The consistent approach of Mr. Sharma showcases the benefits of traditional, low-risk retirement pension plans in India, while Mrs. Iyer’s diversified strategy underscores the potential of combining different types of plans for a more robust financial future.

The paths taken by Mr. Sharma and Mrs. Iyer serve as valuable lessons for anyone embarking on the journey of retirement planning. Whether opting for government retirement plans in India or exploring market-linked options, the crux lies in aligning your investment choices with your financial goals, risk tolerance, and life circumstances.

| Aspect | Mr. Sharma’s Case Study | Mrs. Iyer’s Case Study |

| Occupation | Government Employee | Professional |

| Investment Strategy | Conservative, focusing on safety and steady returns | Diversified, balancing risk with potential for higher returns |

| Primary Investments | Employees’ Provident Fund (EPF) and Public Provident Fund (PPF) | National Pension System (NPS) and Mutual Funds |

| Risk Appetite | Low Risk | Moderate to High Risk |

| Goal of Investment | Stability and guaranteed returns for a secure retirement | Higher returns through diversified investments for a robust retirement corpus |

| Outcome | Substantial corpus ensuring a comfortable and secure retirement | Healthy corpus with a diversified portfolio minimising risks and maximising returns |

| Approach | Consistent long-term saving in traditional, government-backed retirement schemes | Strategic planning with a mix of government-backed and market-linked investments |

| Key Lesson | The power of consistency and starting early in retirement planning | The effectiveness of strategic planning and diversification in investments |

This proves that In retirement planning, there’s no one-size-fits-all solution. It’s about finding the right blend that suits your individual needs, just like a chef mastering a dish with the perfect balance of flavours.

Government Retirement Plans in India: A Detailed Analysis

Government retirement plans stand out as robust, reliable, and integral to the fabric of retirement planning. These schemes, backed by the government, offer a sense of security and stability that is highly valued in the Indian context.

Overview of Key Government-Sponsored Retirement Schemes

Atal Pension Yojana (APY)

Scheme Features:

– Targeted at the unorganised sector, APY aims to provide a steady pension to individuals post-retirement.

– Participants contribute a specific amount monthly, and upon reaching the age of 60, they receive a guaranteed pension.

– Offers pension slabs of INR 1,000 to INR 5,000 per month.

Eligibility and Benefits:

– Open to Indian citizens aged 18-40 years.

– Provides a co-contribution by the Government for eligible subscribers.

– Offers tax benefits under Section 80CCD.

Employees’ Provident Fund (EPF)

Scheme Features:

– A mandatory savings scheme for employees in India, where both employee and employer contribute a fixed percentage of the salary.

– The corpus accumulates over time and earns interest.

– On retirement or resignation, the employee receives the total lump sum, including interest.

Eligibility and Benefits:

– Applicable to organisations with more than 20 employees.

– Provides a high level of security with a steady interest rate.

– Offers tax exemption under Section 80C and tax-free withdrawal.

Public Provident Fund (PPF)

Scheme Features:

– A long-term savings scheme that offers an attractive interest rate and returns that are fully exempt from tax.

– The maturity period of the PPF account is 15 years, which can be extended.

– Offers loan and partial withdrawal facilities after certain conditions are met.

Eligibility and Benefits:

– Open to all Indian citizens.

– Contributions qualify for tax rebate under Section 80C of the IT Act.

– Interest earned and the maturity amount are tax-free.

Comparison with Private Retirement Plans

Contrasting Government and Private Plans

Private retirement plans often provide a wider range of investment options, including equity, debt, and hybrid funds, offering the potential for higher returns compared to traditional government plans. However, they also carry a higher risk, making them suitable for investors with a higher risk appetite.

Private plans often offer more flexibility in terms of contribution, investment choices, and withdrawal options, catering to the dynamic needs of the investor. On the other hand, government schemes are generally more rigid but offer a higher degree of security and predictability.

Evaluating Pros and Cons

Government retirement plans in India, like APY, EPF, and PPF, are foundational elements in the retirement planning process, offering security, stability, and predictable returns. They are particularly suited for individuals who prioritise safety and guaranteed income in their retirement years.

On the other hand, private retirement plans offer higher flexibility and the potential for greater returns, suited for those who are comfortable with higher risk and seek to maximise their retirement corpus.

Here are some pros and cons of these two plans. A detailed table also highlights their differences.

- Risk vs. Return: Government schemes are characterised by their low-risk profile and assured returns, making them a safe haven for conservative investors. Private plans, while offering the potential for higher returns, also come with a higher risk, especially in market-linked plans.

- Tax Benefits: Both government and private retirement plans offer tax benefits, but the nature and extent of these benefits can vary. Understanding the specific tax implications of each plan is crucial in effective retirement planning.

- Liquidity and Flexibility: Private plans typically offer more liquidity and flexibility compared to government schemes. However, this increased flexibility can come at the cost of reduced security and guaranteed returns.

| Feature | Government Retirement Plans | Private Retirement Plans |

| Risk Profile | Generally low risk, offering more security. | Varies; can range from low to high risk. |

| Returns | Fixed and predictable returns. | Market-linked; potential for higher returns. |

| Investment Options | Limited options, primarily in debt instruments. | Wide range of options including equity, debt, and hybrid funds. |

| Flexibility | Less flexibility in terms of contributions and withdrawals. | More flexible with contributions, investment choices, and withdrawals. |

| Tax Benefits | Offers tax benefits under various sections like 80C. | Tax benefits vary; can be under sections like 80C, 80CCD, etc. |

| Suitability | Ideal for conservative investors seeking stability. | Suitable for investors with varied risk appetites, seeking growth. |

| Liquidity | Typically lower liquidity, with some exceptions. | Generally higher liquidity, depending on the plan. |

| Examples | EPF, PPF, APY | Mutual fund-based retirement plans, ULIPs, private pension funds. |

| Guaranteed Income | Often provide guaranteed income post-retirement. | May or may not provide guaranteed income. |

| Plan Structure | More rigid in structure and operations. | Offer greater customization and adaptability. |

| Long-term Security | High, due to government backing. | Depends on market performance and fund management. |

The choice between government and private plans should be based on individual financial goals, risk tolerance, and retirement aspirations. It’s about striking a balance between the safety of government plans and the growth potential of private plans, much like creating a harmonious symphony with different musical instruments.

The best retirement plan is one that is tailored to your unique needs, providing a sense of financial security and peace of mind. As a SEBI Registered Investment Advisor, I advocate for a well-rounded approach to retirement planning, combining the stability of government schemes with the growth potential of private investments, ensuring a retirement journey that is as rewarding as it is secure. Security also means protecting oneself against various risks one could face in retirement planning.

For more information, you can visit: National Pension System (NPS) Official Website: https://www.npscra.nsdl.co.in

Mitigating the Risks in Retirement Planning

Retirement planning can be fraught with various risks. Understanding and mitigating these risks are essential to ensure a comfortable and secure retirement. The journey of retirement planning is not just about accumulating wealth but also about safeguarding it against potential pitfalls. Let’s delve into some of the key risks involved in retirement planning and explore strategies to mitigate them.

1. Sequence of Returns Risk

The sequence of returns risk highlights how the timing of returns impacts your retirement corpus. If you encounter negative returns early in your retirement, it significantly diminishes your portfolio’s ability to bounce back, as you start withdrawing funds when the market is down. This can have a lasting impact on the longevity of your retirement savings.

Mitigation Strategies:

– Diversification: Diversifying your investment portfolio across various asset classes can help spread the risk.

– Regular Rebalancing: Periodically adjusting your portfolio to maintain your desired asset allocation can help manage this risk.

– Early Withdrawals: Starting withdrawals from your investments early in retirement can reduce your dependence on them later, especially during market downturns.

2. Inflation Risk

Inflation reduces the value of money over time, thereby diminishing the purchasing power of your retirement corpus. In a country like India, with relatively high inflation rates, this risk can significantly impact retirement planning.

Mitigation Strategies:

– Investing in Inflation-Protected Securities: Consider investing in instruments that offer returns aligned with inflation rates.

– Growth-Oriented Investments: Including assets that have the potential to outpace inflation, like equities, can be beneficial.

3. Longevity Risk

With increasing life expectancy, there’s a real risk of outliving your retirement savings. This risk is amplified with the rising cost of healthcare and living expenses.

Mitigation Strategies:

– Annuity Plans: Investing in annuity plans that offer a lifetime income can help mitigate this risk.

– Additional Savings: Increasing your savings rate during your working years can provide a larger corpus to draw from during retirement.

4. Health Care Risk

Healthcare costs are escalating rapidly, and unexpected medical expenses can deplete your retirement savings.

Mitigation Strategies:

– Health Insurance: Maintaining adequate health insurance coverage is crucial.

– Emergency Fund: Creating a dedicated emergency fund for medical expenses can provide a financial cushion.

5. Market Risk

Market risk refers to the potential loss due to the volatile nature of investment markets. This risk is particularly significant for retirement portfolios heavily invested in equities.

Mitigation Strategies:

– Asset Allocation: A balanced asset allocation based on your risk tolerance can help manage this risk.

– Regular Monitoring: Keeping a close eye on market trends and adjusting your investment strategy accordingly is essential.

6. Policy Risk

Policy risk involves uncertainty due to changes in government policies, taxation, and retirement benefits, which can affect your retirement planning.

Mitigation Strategies:

– Stay Informed: Keeping abreast of policy changes and adjusting your retirement plan accordingly is crucial.

– Professional Advice: Seeking advice from financial experts can help navigate through policy changes.

7. Withdrawal Rate Risk

Withdrawal rate risk occurs when you withdraw too much from your retirement fund too quickly, risking depleting your savings prematurely.

Mitigation Strategies:

– Sustainable Withdrawal Rates: Adhering to a sustainable withdrawal rate based on your total corpus and life expectancy is important.

– Flexible Spending Plans: Adjusting your spending based on the performance of your investments can help manage this risk.

Yes, retirement planning in India comes with its set of risks – from the sequence of returns and inflation to longevity and market risks. Navigating these risks requires a well-thought-out strategy that includes diversification, regular rebalancing, adequate insurance, and staying informed about policy changes. Working with a financial advisor can provide tailored advice and help you create a retirement plan that not only grows your wealth but also protects it against these risks.

Conclusion

To sum up, the art of retirement planning in India is similar to crafting a personalised masterpiece, tailored to your life’s unique journey. It’s a process that demands attention to detail, an understanding of the broader picture, and a careful blend of various financial instruments. The objective is not just to weave a safety net for the future but to create a plan that reflects your aspirations and dreams, ensuring that your retirement years are as vibrant and fulfilling as the preceding ones.

The approach to retirement planning should also be like nurturing a tree, where patience, care, and foresight are essential. It’s not merely about planting the seed; it’s about regular nurturing, adapting to changing conditions, and ensuring robust growth. The Roots and Wings investment philosophy plays a pivotal role in this context. It advocates for investments in companies with strong fundamentals (Roots) – those with solid balance sheets, high return on equity, and top-notch management. Simultaneously, it focuses on companies exhibiting growth potential (Wings) – characterised by consistent revenue and profit growth, and market leadership. This dual focus ensures a balanced approach, mitigating risks while providing growth opportunities.

In terms of asset allocation, the LSG (Liquidity, Safety, Growth) framework of Jama Wealth offers a structured approach. It helps in aligning investments with your risk profile, ensuring that your portfolio is well-diversified across different asset classes, thus reducing risk and optimising returns. This prudent allocation is essential, as it balances the need for immediate liquidity, ensures safety of capital, and fosters long-term growth.

Embrace the wisdom of Warren Buffet: “Do not save what is left after spending, but spend what is left after saving.” This philosophy is central to successful retirement planning. It emphasises the importance of prioritising savings and investments, ensuring financial security and peace of mind in the later years of life. However, retirement planning is more than just accumulating wealth; it’s about creating a future that continues to enrich your life with experiences and fulfilment. It’s about finding that sweet spot between saving for tomorrow and enjoying today.

In this quest, Jama Wealth’s Portfolio Management Services and associated investment advisory services can help guide you through the complexities of financial planning and investment management. These services ensure that your journey towards retirement is not just secure but also rewarding.

The practical steps in this journey begin with an honest assessment of your current financial situation, followed by setting clear, achievable retirement goals. Regular reviews and adjustments of your financial plan are crucial, as they help your strategy stay aligned with life changes, economic shifts, and personal goals. Most importantly, selecting a retirement plan that resonates with your personal aspirations and risk tolerance is key. Successful retirement planning is not just about how much you save but also about how well you manage and protect those savings against potential risks.

It is never too early or too late to start planning for retirement. Each decision you make today is a step towards securing a more prosperous and fulfilling future. Your future self will indeed be grateful for the foresight and wisdom you exhibit today. With the right plan, disciplined approach, and a trusted advisor by your side, your retirement can indeed become the most rewarding and enriching chapter of your life.