The Indian financial markets offer a plethora of investment opportunities. From bustling equity markets to reliable government bonds, the diversity is as vast as the country itself. As Indian investors become more financially literate, they are increasingly exploring a variety of investment avenues. This blog specifically talsk about asset allocation.

In this evolving financial landscape, asset allocation has emerged as a critical element of investment strategy. It’s not just about picking the right stocks or bonds or mutual funds; it’s about creating a balanced portfolio that aligns with one’s financial goals and risk tolerance. As Warren Buffett rightly said, “Do not put all your eggs in one basket.” This principle holds true in the dynamic Indian market as well.

Understanding Asset Allocation: A Deep Dive

Asset allocation is an integral component of the investment strategy, particularly in the diverse and dynamic Indian financial landscape. Let’s delve deeper into its definition, significance, and historical context in India, along with exploring various facets that make it a crucial element in financial planning.

Definition and Significance in the Indian Context

Asset allocation is the process of distributing investments across various asset classes such as equities, bonds, real estate, and gold. It’s about creating a balanced portfolio that aligns with an investor’s risk tolerance, investment goals, and time horizon. In India, where investment choices are influenced by cultural and economic factors, asset allocation becomes pivotal in achieving financial stability and growth.

Just as a well-prepared thali offers a mix of flavours and nutrition, a well-diversified investment portfolio balances risk and return. Each asset class in the portfolio plays a unique role, akin to the different dishes in a thali, contributing to the overall financial health of the investor.

Historical Context of Asset Allocation in India

Traditionally, Indian investors have shown a strong preference for gold and real estate, viewing them as safe and tangible assets. These investments were perceived as hedges against inflation and economic uncertainty.

The liberalisation of the Indian economy in the 1990s marked a significant shift in investment patterns. The introduction of new financial instruments like equities and mutual funds broadened the investment horizon for Indian investors, offering higher returns albeit with increased risk.

The Evolution of Asset Allocation Strategies

The advent of Modern Portfolio Theory (MPT) in asset management lifecycle has had a profound impact on asset allocation. It advocates for diversification to reduce risk while optimising returns, a concept that has become increasingly relevant in the Indian context.

The concept of tailoring asset allocation according to an investor’s age and risk appetite gained prominence. Younger investors with a longer time horizon and higher risk tolerance might lean more towards equities, while older investors prioritise stability and income through bonds or fixed-income assets.

Asset Allocation Tools and Calculators

With technological advancements, various online tools and calculators have become available for investors. These tools help determine an appropriate asset mix based on individual risk profiles and financial goals.

Asset allocation calculators have simplified the process of portfolio planning, making it more accessible for the average Indian investor to make informed decisions.

Understanding and implementing an effective asset allocation strategy is essential for investors in the Indian market. With its roots in traditional preferences and evolving with global investment practices, asset allocation in India has become a sophisticated and necessary approach for wealth creation and risk management. Whether through direct investment choices or through structured systems like PMS, Lifecycle Funds, and NPS, asset allocation continues to play a crucial role in shaping the financial futures of Indian investors.

Why Asset Allocation Matters: Diversification and Risk Management in the Indian Market

In the ever-evolving landscape of the financial markets, asset allocation emerges as a critical strategy for investors. This comprehensive approach to investing is not just about wealth creation; it’s about building a resilient portfolio that can withstand market volatility while optimising returns.

Diversification in asset allocation is about spreading investments across various asset classes such as equities, debt, real estate, and gold. This strategy is akin to a farmer planting multiple types of crops, thereby reducing the dependence on the success of just one crop. In the financial world, diversification helps in mitigating risks associated with the performance of a single asset class.

There are various asset allocation strategies, including strategic, tactical, and dynamic allocation. Each strategy offers a different approach to diversification, catering to diverse investor profiles and goals.

The asset allocation portfolio should include a mix of growth-oriented and stable investments. While equities offer higher growth potential, debt instruments like bonds provide stability. Real estate and gold serve as hedges against inflation and market volatility.

Factors Shaping Asset Allocation Decisions for Indian Investors

Asset allocation is an essential consideration for investors aiming to navigate the complexities of wealth creation and management effectively. In the Indian context, asset allocation decisions are influenced by a blend of cultural, economic, and individual factors.

Cultural and Economic Influences on Asset Allocation

1. Traditional Preferences

The Indian investment ethos is steeped in tradition, with gold and real estate historically perceived as cornerstones of security and prosperity. These assets are often passed down through generations, signifying wealth and stability.

2. Economic Shifts

India’s economy has undergone significant transformation, opening up new avenues for investment beyond traditional assets. The liberalisation of markets and the advent of diversified financial instruments have expanded the Indian investor’s portfolio choices.

3. Influence of Socio-Economic Factors

Socio-economic developments, such as rising middle-class affluence and digital financial inclusion, have also played a role in shaping investment patterns, encouraging a shift towards equities and mutual funds.

Understanding Risk Tolerance in Asset Allocation

1. Risk Appetite of Indian Investors

Indian investors’ risk tolerance is shaped by a variety of factors, including age, income levels, and life goals. A young professional may be more inclined towards equities for long-term growth, while retirees may prioritise capital preservation.

2. Asset Allocation by Age

Age-based asset allocation is a strategy that aligns investment choices with the investor’s life stage. Younger investors may adopt a more aggressive asset allocation strategy, whereas older investors may seek more conservative asset mixes.

3. The Importance of Asset Allocation

Effective asset allocation is vital for risk management and capital appreciation. It helps investors balance their desire for wealth accumulation with the need for financial security.

Asset Allocation Strategies for Indian Investors

1. Strategic Asset Allocation

This approach involves setting target allocations for various asset classes and periodically rebalancing the portfolio to maintain these targets. It’s a disciplined strategy that aligns with long-term investment objectives.

2. Dynamic Asset Allocation

In contrast to a static strategy, dynamic asset allocation allows for adjusting the asset mix in response to market conditions, aiming to capitalise on market trends while managing risk.

3. The Role of Asset Allocation Mutual Funds

Asset allocation mutual funds offer a convenient way for investors to achieve a diversified portfolio. These funds automatically adjust their asset mix, providing a balanced investment approach suited to the investor’s risk profile.

Tailoring Asset Allocation to Individual Needs

1. Personal Financial Goals

Investors’ personal financial goals play a crucial role in shaping their asset allocation. Whether saving for a child’s education, buying a home, or planning for retirement, each goal may require a different asset mix.

2. Economic Environment

The prevailing economic environment also impacts asset allocation decisions. Factors such as interest rates, inflation, and economic growth can influence the attractiveness of various asset classes.

Asset allocation in India is a nuanced process, influenced by an array of factors from cultural preferences to economic conditions. By understanding these influences and leveraging available tools and strategies, Indian investors can construct portfolios that not only reflect their unique risk profiles but also position them well for achieving their investment goals. With the right asset allocation strategy, investors can enjoy the dual benefits of portfolio growth and risk mitigation, essential for long-term financial success.

Crafting an Effective Asset Allocation Strategy for Indian Investors

Crafting an effective asset allocation strategy is pivotal for achieving financial success. Asset allocation is the bedrock of a sound investment plan, determining the trajectory of an investor’s journey towards their financial aspirations.

- The Pillars of Goal-Based Asset Allocation

Investors must align their asset allocation with specific financial objectives. This ensures that each investment serves a purpose, whether it’s funding a child’s education, purchasing a home, or providing for a comfortable retirement. Let us elaborate on these two further.

In retirement planning, a SEBI Registered Investment advisor might recommend starting with a growth-oriented asset allocation fund and gradually shifting to more conservative investments as retirement nears.

For education funding, the advisor may suggest a mix of asset allocation mutual funds that offer the potential for growth while managing risks as the time to draw on the funds approaches.

- Time Horizon as a Guiding Force

For goals within a short timeframe, investors might consider more liquid and less volatile asset classes, like money market funds or short-term bonds.

For longer-term goals, a portfolio weighted towards equities may be appropriate, given their potential for higher returns over time.

- Asset Management Lifecycle Considerations

Lifecycle Funds adjust the asset allocation mix as the investor ages, shifting from growth-oriented investments to more conservative options automatically.

Investors can also follow a Customised Asset Allocation Strategy by working with SEBI registered investment advisors to create a personal asset allocation strategy that adjusts over time based on their changing life circumstances and financial goals.

- Navigating Asset Allocation Types

While strategic asset allocation sets a long-term investment strategy, tactical asset allocation allows investors to make short-term deviations from the asset mix to capitalise on market opportunities or mitigate risks.

Asset allocation calculators have become invaluable for investors seeking to tailor their portfolios to their risk profiles and financial targets.

- Diversification as a Necessity

Diversification is essential in any asset allocation strategy, spreading investments across various asset classes to mitigate risks and improve potential returns.

An effective asset allocation strategy is critical for Indian investors seeking to build and preserve wealth. It requires a delicate balance between managing risks and aiming for growth, tailored to individual goals and life stages. By employing various asset allocation types, understanding the importance of time horizons, and utilising tools like asset allocation calculators, investors can craft a portfolio that not only meets their financial objectives but also adapts to the economic landscape of India. With the support of a SEBI Registered Investment advisor, investors can navigate the asset management lifecycle with confidence and precision, ensuring that their investment decisions lead to a prosperous financial future.

A well-considered asset allocation strategy reduces risk by not overexposing the portfolio to any single asset class or market fluctuation. By including growth assets like equities in the asset mix, investors can benefit from capital appreciation, which is essential for outpacing inflation and building wealth.

Navigating Different Asset Classes in the Indian Market

Investors are presented with an array of asset classes, each holding different characteristics and growth potentials. Going through these options requires an informed asset allocation strategy, a pivotal factor in the asset management lifecycle that can greatly influence investment outcomes.

Overview of Popular Asset Classes in India

1. Equities for Growth: Equities are often the go-to asset class for investors looking for growth. They represent ownership in companies and carry the potential for high returns through capital gains and dividends. Equities are suitable for investors who can stomach market volatility in pursuit of higher returns.

2. Debt Instruments for Stability: Bonds and other debt instruments provide a more stable income stream, typically attracting investors seeking regular interest payments and the preservation of capital. They act as a counterbalance to the volatility of equities in an asset allocation portfolio.

3. Real Estate for Tangible Value: Real estate investments in India have traditionally been favoured for their tangible nature and perceived long-term value appreciation. They also offer rental income potential and can serve as a hedge against inflation.

Strategies for Diversifying Across Asset Classes

1. Creating a Balanced Portfolio: A balanced portfolio in the Indian market could include equities for long-term growth, debt instruments for steady income, and real estate for diversification and potential appreciation. This mix can help mitigate risks while providing the opportunity for capital appreciation.

2. Asset Allocation Mutual Funds: For those seeking diversified exposure without managing individual investments actively, asset allocation mutual funds can be an excellent option. These funds automatically adjust their asset mix based on market conditions and the fund manager’s outlook.

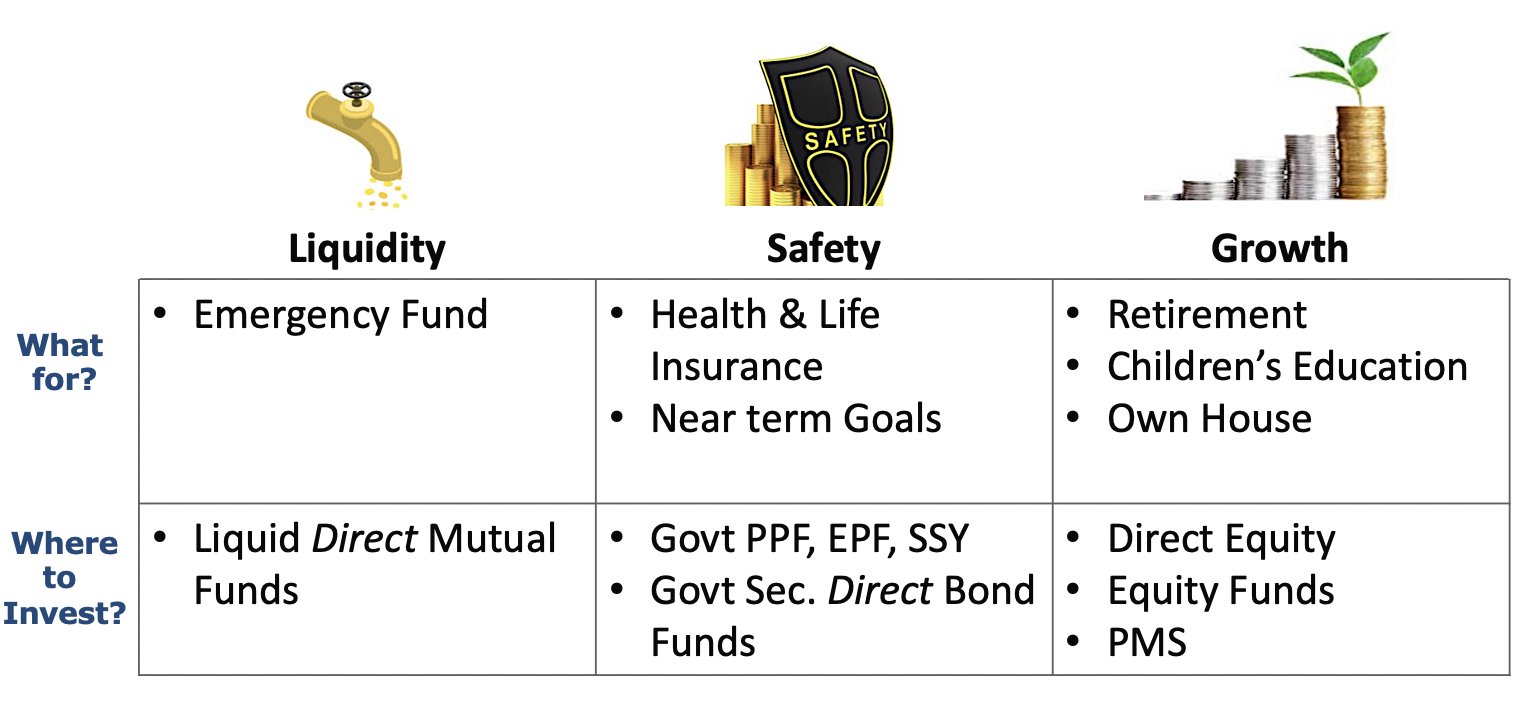

3. Consider the Liquidity-Safety-Growth Framework: This is elaborated in the section below.

Investors can utilise asset allocation calculators to assist in determining an appropriate mix of investments. These tools consider factors such as age, risk tolerance, financial goals, and investment horizon to suggest an asset allocation strategy.

Asset Allocation Benefits and Advanced Strategies

1. Long-Term Wealth Creation: Proper asset allocation is key to long-term wealth creation. It ensures that investments are spread across asset classes that can perform well in different market conditions.

2. Dynamic Asset Allocation: This advanced strategy involves actively adjusting the asset mix in response to short-term market movements. It requires a keen understanding of market dynamics and can potentially enhance portfolio returns if executed correctly.

To sum up, navigating the different asset classes in the Indian market is an art that requires a deep understanding of each class’s nuances. By employing a disciplined asset allocation strategy, Indian investors can build a portfolio that balances risk with the potential for growth.

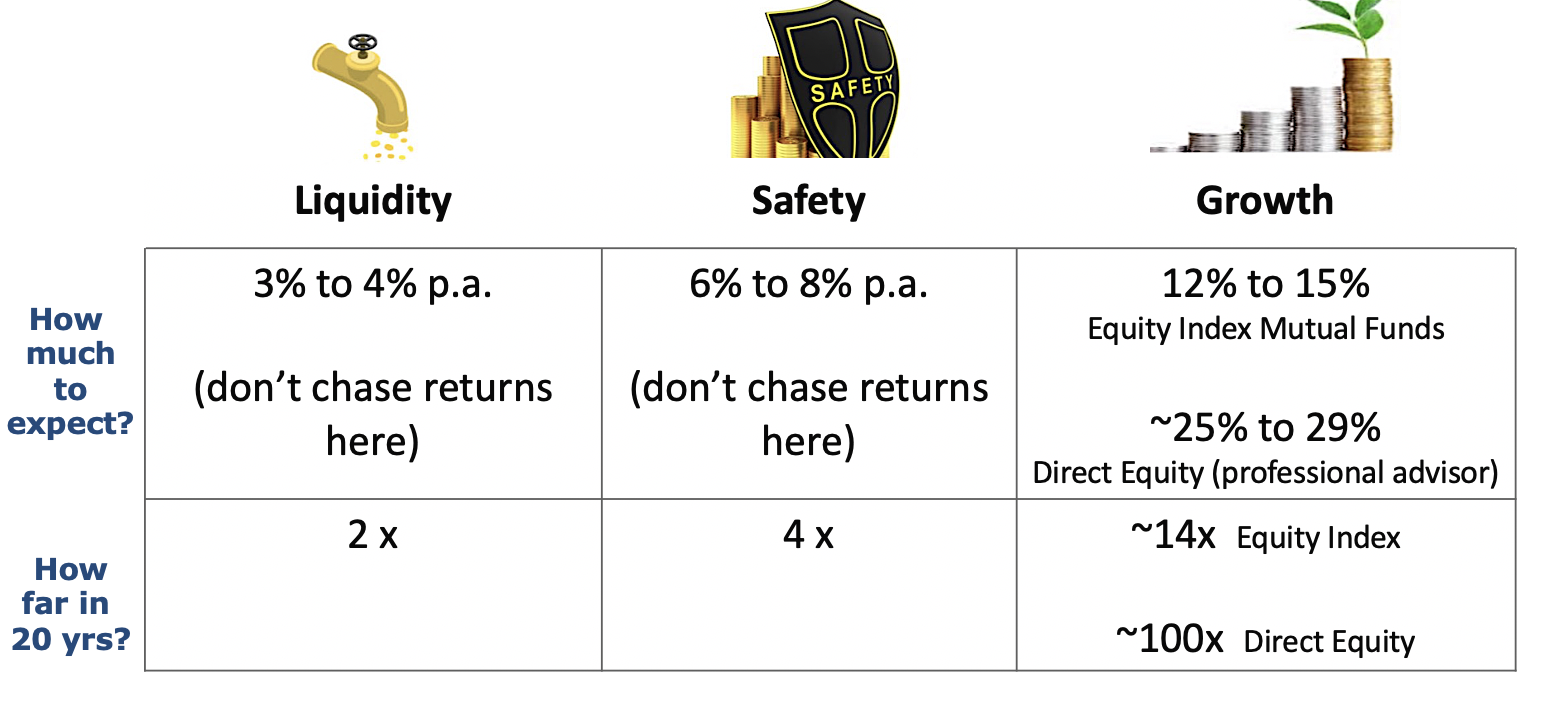

The LSG Framework of Jama Wealth as a Pragmatic Approach for Asset Allocation

The LSG (Liquidity, Safety, Growth) framework emerges as a cornerstone principle for astute asset allocation in the quest for financial stability and growth. This robust approach balances immediate cash needs, the preservation of capital, and the pursuit of capital appreciation, encapsulating the essence of a well-rounded investment strategy.

Liquidity: Ensuring Accessible Cash Reserves

1. Immediate Cash Needs: Liquidity is about having funds available when you need them. In asset allocation, it means keeping a portion of your portfolio in assets that can be quickly and easily converted into cash.

2. Importance in Asset Allocation: An investor’s liquidity needs should dictate the initial layer of their asset allocation strategy. This often includes keeping money in savings accounts, money market funds, or short-term fixed-income securities that offer quick access and minimal impact from market fluctuations.

Safety: The Preservation of Capital

1. Minimising Risks: Safety focuses on protecting the investment capital from potential losses. This involves allocating assets to investment vehicles offering lower risk and more predictable returns, such as government or high-grade corporate bonds.

2. Role in Portfolio Balance: In the asset allocation mix, safety counterbalances more volatile investments. It ensures that a portion of the portfolio is shielded from the inherent risks of the market, providing a stable foundation for the investor’s wealth.

Growth: Capital Appreciation for the Long Term

1. Pursuing Higher Returns: Growth is the aspect of asset allocation aimed at increasing the investor’s capital over the long term. This typically involves investing in equities, which carry higher risk but offer the potential for higher returns compared to fixed-income assets.

2. Strategic Allocation for Growth: The growth component of the LSG framework is tailored to an investor’s risk tolerance and time horizon. It often includes a mix of individual stocks, equity mutual funds, or growth-oriented asset allocation funds that can provide the benefit of compounded returns over time.

Integrating the LSG Framework in Asset Allocation

1. A Holistic Investment Strategy: The LSG framework guides investors in creating a diversified portfolio that reflects their financial situation and goals. The framework provides a strategic foundation for asset allocation decisions by incorporating liquidity, safety, and growth.

2. Flexibility and Personalization: The LSG framework is not rigid; it allows for flexibility based on individual circumstances. For instance, an investor closer to retirement may emphasise safety and liquidity, while a younger investor may focus on growth to maximise long-term returns.

The LSG Framework and Asset Allocation Funds

1. Asset Allocation Funds as a Vehicle: Many asset allocation mutual funds inherently follow the LSG framework by offering a balanced mix of stocks, bonds, and other assets. These funds manage the allocation ratios internally, adjusting the portfolio to align with market conditions and the fund’s investment objectives.

2. Benefits for Investors: Investors benefit from the LSG framework’s integrated approach when using these funds. They can achieve a diversified portfolio that caters to liquidity needs, prioritizes safety, and seeks growth, all within a single investment vehicle.

To sum up, the LSG framework is a pragmatic tool that can profoundly influence asset allocation, ensuring that investors’ portfolios are well-equipped to meet their financial needs at different life stages. It encapsulates the principles of prudent investing, providing a clear structure for balancing the competing demands of accessibility, security, and profitability. Whether applied to individual asset choices or through asset allocation funds, the LSG framework is instrumental in empowering investors to build robust and resilient investment portfolios.

Tailoring Asset Allocation to Indian Demographics

Asset allocation is a vital component of financial planning, crucial in crafting a portfolio that resonates with an investor’s life stage, financial goals, and risk tolerance. In India, where demographic factors significantly influence investment choices, tailoring asset allocation strategies becomes particularly essential.

Age-Based Allocation Strategies: Customizing Investments Across Life Stages

In the Indian investment context, age is not just a number; it’s a pivotal factor that influences how asset allocation is structured. The asset management lifecycle for an investor begins with understanding that each phase of life requires a different investment approach.

1. The Youthful Investor: For the younger demographic, typically in their 20s and 30s, financial advisers often recommend a strategy leaning towards equities. This asset allocation type takes advantage of the long-term horizon, harnessing the market’s growth potential to build wealth over time. The concept here is simple: with more time to ride out market volatility, younger investors can afford to take on more risk for greater returns.

2. Middle Age Prudence: As investors enter their 40s and 50s, the asset allocation strategy often shifts. At this stage, balancing growth with risk management becomes crucial. The asset allocation portfolio may still include a significant proportion of equities, but with a greater emphasis on debt instruments and other asset allocation funds that provide a cushion against market downturns.

3. Retirement Readiness: For those nearing retirement, stability and income generation take centre stage. Asset allocation mutual funds and debt securities become more prominent, reflecting a conservative approach. The aim is to preserve capital and ensure a steady income stream, aligning the asset allocation portfolio with the need for financial security during retirement.

Role of Life-Cycle Funds: Automating Asset Allocation for Seamless Transitions

Life-cycle funds have emerged as a popular tool in the Indian market, offering a seamless asset allocation strategy that evolves with the investor’s age.

1. Adapting with Age: These funds are designed to automatically become more conservative as the investor approaches retirement age. For instance, a life-cycle fund might start with an aggressive asset allocation portfolio, primarily equities and gradually shift to a conservative mix with a higher allocation to bonds and fixed-income assets.

2. Simplicity and Convenience: The appeal of life-cycle funds lies in their simplicity. Investors can select a fund based on their target retirement age and let the fund managers adjust the asset allocation strategy over time. This approach eliminates the need for investors to regularly rebalance their portfolios, making it a convenient option for those seeking a hands-off investment strategy.

To sum up, tailoring asset allocation according to Indian demographics is not just a good strategy; it’s essential for financial well-being. It ensures that investments are not just parked but are actively working towards the realisation of life goals. Whether one opts for individual asset selection, life-cycle funds, or national schemes like the NPS, a well-thought-out asset allocation strategy’s benefits are manifold, promising wealth preservation and the potential for growth and prosperity.

Indian Case Study: Optimal Asset Allocation for Long-Term Wealth Creation

The tale of a middle-aged Indian investor illustrates the profound impact of a meticulously crafted asset allocation strategy. This strategy is bolstered by the prudent application of the LSG (Liquidity, Safety, Growth) framework, which serves as a guiding principle throughout the asset management lifecycle.

Initial Portfolio Composition: Equity-Weighted for Growth

1. Growth-Focused Beginning: Our investor’s journey begins with a portfolio heavily weighted in equities. This asset allocation choice is driven by the pursuit of growth — a common strategy for those with a longer time horizon to capitalise on the higher potential returns of the stock market.

2. Equities in the Asset Allocation Fund: Within this equity-heavy portfolio, a substantial allocation is directed towards asset allocation mutual funds, which offer diversified exposure to a range of Indian stocks, from blue-chip companies to burgeoning start-ups poised for growth.

Transitioning Strategy: Balancing the Portfolio with Debt and Fixed Income

1. Asset Allocation by Age: As the investor progresses through the asset management lifecycle, the need for stability becomes more pronounced. Recognizing the importance of asset allocation, the strategy evolves, gradually shifting towards debt instruments and fixed-income assets.

2. Incorporating the LSG Framework: Liquidity is maintained through investments in liquid funds and short-term money markets, ensuring that immediate cash needs can be met without disrupting the long-term investment strategy. Safety is enhanced by adding government and high-grade corporate bonds to the portfolio, providing stable returns and preserving capital. Growth remains a component, albeit more measured, with a reduced but still significant allocation to equities.

Diversification and Stability: Real Estate and Gold

1. Real Estate for Long-Term Value: A portion of the portfolio is dedicated to real estate investments. This not only aligns with traditional Indian investment preferences but also serves as a tangible asset with the potential for both rental income and capital appreciation.

2. Gold as a Safe Haven: Gold, revered in Indian culture, is included for its historical role as a safe haven and a hedge against inflation. It complements the fixed-income assets, further diversifying the portfolio and adding a layer of safety.

This case study encapsulates the essence of strategic asset allocation in India, blending traditional investment wisdom with modern financial tools and frameworks. It illustrates how the LSG framework can serve as a guide throughout the asset allocation journey, ensuring that each stage of the investor’s life is supported by a portfolio that is robust, responsive, and resilient.

Advanced Asset Allocation Strategies for Indian Investors

In the fast-paced world of finance, investors who harness advanced asset allocation strategies position themselves well for navigating market volatility while capitalising on growth opportunities. Such strategies are not static but dynamic, evolving with market conditions and personal financial milestones.

Dynamic Asset Allocation: Adapting to Market Movements

Dynamic asset allocation is a proactive strategy that allows investors to adjust their portfolio’s asset mix in response to changing market conditions. This method demands an active approach to portfolio management, with decisions based on short-term market trends and long-term financial objectives.

In practice, dynamic asset allocation might involve increasing equity exposure during a bull market to maximise returns or shifting towards bonds and fixed-income instruments in anticipation of a market downturn. It requires a keen understanding of market indicators and the agility to act upon them.

Insights into Various Asset Allocation Strategies

1. Constant-Weight Allocation: The constant-weight strategy is grounded in maintaining a fixed asset allocation ratio. When market movements cause a deviation from the predetermined balance, the portfolio is rebalanced accordingly. This approach ensures discipline in investment, helping investors stay aligned with their risk tolerance and investment goals.

2. Tactical Asset Allocation: Tactical asset allocation takes a more opportunistic approach, allowing for temporary adjustments to the asset mix to exploit market inefficiencies or strong market sectors. It’s a strategy that combines the long-term perspective of strategic asset allocation with the flexibility to capitalise on short-term market opportunities.

3. Insured Asset Allocation: Insured strategies aim to protect the portfolio from significant losses. This approach sets a base portfolio value below which the portfolio should not fall, and if the market drops to this level, the portfolio is reallocated to avoid further losses, often shifting to less risky assets.

Implementing Advanced Strategies in the Indian Market

1. Market Trends and Investor Profiles: Adapting these advanced strategies to the Indian market requires an intimate knowledge of local market trends and investor profiles. Indian investors must consider domestic market indicators, economic policies, and global events that can impact local assets.

2. Risk and Return Considerations: Each advanced strategy offers a different method for balancing risk and return. Indian investors need to assess their personal risk appetite and the potential impact on their portfolios before adopting a specific advanced asset allocation strategy.

The Role of Asset Allocation Mutual Funds

1. Professional Management: Asset allocation mutual funds in India often employ these advanced strategies, managed by professional fund managers who make allocation decisions on behalf of investors. This option can be particularly appealing for investors who prefer not to manage these complex strategies on their own.

2. Diverse Strategies Under One Umbrella: Such mutual funds provide exposure to a range of strategies, from dynamic to tactical, enabling investors to benefit from a diversified approach to asset allocation within a single investment vehicle.

To sum up, advanced asset allocation strategies offer Indian investors a sophisticated set of tools to enhance portfolio performance and manage risk. By employing dynamic, tactical, or insured approaches, investors can navigate the complexities of the Indian market more effectively. As with any investment strategy, the key lies in choosing an approach that aligns with individual financial goals, time horizons, and risk tolerance. With the right strategy in place, investors can aspire not only to preserve capital but also to grow it, ensuring their financial well-being in the ever-changing landscape of the Indian economy.

Rebalancing is Crucial to make Asset Allocation Successful

If one is looking for shock absorbers in the rollercoaster ride of investing, then rebalancing offers that comfort. Re-balancing, in simple terms, is about sticking to one’s asset allocation. Let us take an example here to illustrate this. Mr. A might allocate his funds across the 4 asset classes as under Equity 45%, Long term Debt 30%, Short Term Debt 15%, and Gold 10%.

Once Mr. A has invested let us say, Rs.100,000 across the 4 asset classes in the proportion mentioned above, his money will start growing at different rates. Let us assume that, during a period of 1 year, Equity gave a return of 20%, Long Term Debt 8%, Short term Debt 6%, and Gold gave a negative return of 2%. His portfolio will now look as under:

| S.No | Asset Class | Amount invested | Asset Allocation | Return | Amount after 1 year | Asset Allocation |

| 1 | Equity | 45000 | 45% | 20% | 54000 | 48% |

| 2 | LT Debt | 30000 | 30% | 8% | 32400 | 29% |

| 3 | ST Debt | 15000 | 15% | 6% | 15900 | 14% |

| 4 | Gold | 10000 | 10% | -2% | 9800 | 9% |

| 100000 | 112100 |

When Mr. A reviews the portfolio, he is happy that he invested a larger amount in Equity as Equity gave the highest return of 20% p.a. However, he is unhappy that his overall portfolio gave a return of only 12.1%, whereas if he had invested the entire amount in Equity, he would have earned 20% or Rs.20,000.

At this point in time, the tendency is to get out of other Asset classes such as LT Debt, ST Debt, and Gold, and invest the entire amount in equity. However, investors who have learned the lesson of diversification may not do that and allow the portfolio to remain as is.

Even if Mr. A leaves the portfolio as is, kindly note that the asset allocation has changed. Equity is now 48% of the portfolio. The proportion of LT Debt and ST Debt has fallen to 29% and 14% respectively, whereas Gold constitutes only 9% of total assets.

Let us extend this scenario to another 4 years, although it may not be possible to achieve the same returns year after year. After 5 years, Mr.A’s portfolio will be as under:

| S.No | Asset Class | Amount after 5 years | Asset Allocation |

| 1 | Equity | 1,11,974 | 60% |

| 2 | LT Debt | 44,080 | 24% |

| 3 | ST Debt | 20,073 | 11% |

| 4 | Gold | 9,039 | 5% |

| 1,85,167 |

Nothing wrong with that, except that Equity is now 60% of the total portfolio, as opposed to the original asset allocation of 45%. Is that a problem? Let us assume that year 6 experiences global turmoil and there is a 40% fall in equities, Debt continues to earn the same rates but Gold has shot up by 20%. Mr. A’s portfolio at the end of the 6th year would be as under:

| S.No | Asset Class | Amount after 5 years | 6th year returns | Amount after 6 years | |

| 1 | Equity | 1,11,974 | 40% | 67,185 | 46% |

| 2 | LT Debt | 44,080 | 8% | 47,606 | 32% |

| 3 | ST Debt | 20,073 | 6% | 21,278 | 14% |

| 4 | Gold | 9,039 | 20% | 10,847 | 7% |

| 1,85,167 | 1,46,916 |

Nothing wrong with that apparently. However, if one were to look at returns earned over the period and more importantly if one of the financial goals were to be met during the 6th year, there could be a huge setback due to a sudden fall in equities in the 6th year. This is because we did not rebalance the portfolio every year.

Periodic Rebalancing Guides You to Your Goals

In our example, the asset allocation at the beginning and end of the first year changed, as the returns varied across different asset classes. Out of the total portfolio value of Rs.1,12,100, equity is Rs.54,000, whereas as per the asset allocation plan of Mr.A, it should be only 45%. Having adequate liquidity ready for your goals is very important here.

In other words, in a portfolio of Rs.112,100, equity at 45% should be Rs.50,445 (45% of Rs.112,100). Thus, equity is more to the extent of Rs.3,555. As part of rebalancing, Mr.A needs to sell equity to the extent of Rs.3,555. Similarly, Gold, which should have been 10% of the portfolio, or Rs.11,210 in value is only Rs.9,800. The investor needs to buy Gold to the extent of Rs.1,410.

This table explains the Rebalancing to be done:

| S.No | Asset Class | Amount invested | Asset Allocation | Return | Amount after 1 year | As per asset allocation | Action to be taken | |

| 1 | Equity | 45,000 | 45% | 20% | 54,000 | 50,445 | Sell Equity | -3,555 |

| 2 | LT Debt | 30,000 | 30% | 8% | 32,400 | 33,630 | Buy LT Debt | 1,230 |

| 3 | ST Debt | 15,000 | 15% | 6% | 15,900 | 16,815 | Buy ST Debt | 915 |

| 4 | Gold | 10,000 | 10% | -2% | 9,800 | 11,210 | Buy Gold | 1,410 |

| 1,00,000 | 1,12,100 | 0 |

Rebalancing Enforces Discipline

Contrary to the general investor behaviour of investing more in asset classes that yield higher returns, rebalancing forces the investor to sell or redeem assets that have given higher returns and buy assets that have given a lower return. This is an example of rupee cost averaging. Thus, over a period of time, one accumulates more at lower levels and actually books profits at higher levels, resulting in higher overall long-term returns.

Of course, rebalancing as a strategy may appear too conservative if an asset class is on a continuous upward trajectory, giving supernormal returns year after year. However, even in this case, the original asset allocation is always maintained, and the investor does not lose much. It is just that she could have made more by having a higher allocation to such an asset.

Unfortunately, we do not know in advance how the asset class is going to perform. We do know that most of the time, returns from any asset class are not consistently above or below “average market returns.” In this situation, rebalancing not only protects our gains but also enhances overall portfolio returns.

How Often to Rebalance?

It is recommended that this exercise is carried out at least once annually or when the investor feels that there is a significant change in circumstances. Investors must guard against knee-jerk reactions and certain macro events and rush to make changes in their allocation.

It is recommended that an investor not only rebalances the portfolio as per his/ her asset allocation but also takes the opportunity to review his/her portfolio in the light of the change in circumstances from the time the allocation was earlier done to the time of review.

Within a stock portfolio a more frequent rebalancing such as quarterly may be required because of event such as quarterly result announcements. This also depends on the investment strategy being followed.

The Role of Asset Allocation in India’s National Pension System (NPS)

India’s National Pension System (NPS) is a good testament to the critical role of asset allocation in securing a financially stable retirement. NPS is not just a retirement saving avenue; it is a strategic framework offering structured asset allocation to cater to the diverse risk appetites of its vast subscriber base.

NPS Framework: A Versatile Spectrum of Asset Allocation

1. Choice and Control: The NPS framework empowers subscribers with choices that range from conservative to aggressive asset allocation. This flexibility is significant because it allows individuals to tailor their retirement portfolios according to their comfort with market volatility and their financial goals.

2. Risk-Based Options: The system offers different schemes, categorically labeled from E (equity) to G (government securities), with varying degrees of risk and return profiles. Subscribers can decide how much of their pension corpus to allocate to each asset class, with the option to adjust these allocations as their risk appetite or market conditions change.

3. Tiered Structure: NPS operates with a two-tier structure: Tier I being the primary account with tax benefits and restrictions on withdrawal, and Tier II functioning as a voluntary savings facility with more flexibility. This tiered approach allows for varied asset allocation strategies within the same pension framework.

Alignment with Broader Asset Allocation Principles

1. Diversification: NPS’s asset allocation options are designed to diversify a subscriber’s retirement savings across equities for growth, corporate bonds for higher income than government bonds, and government securities for capital protection. This diversification mirrors the broader asset allocation principles that advocate for spreading investments to manage risk and optimise returns.

2. Lifecycle Funds: In alignment with the lifecycle asset allocation strategy, NPS offers a default option that automatically adjusts the equity exposure based on the subscriber’s age. As the subscriber ages, the fund systematically reduces equity exposure, shifting towards more conservative assets like government securities.

The Benefits of NPS in Retirement Planning

1. Structured Asset Allocation: NPS facilitates a structured approach to retirement planning through its pre-defined asset allocation strategies. It reduces the complexity for individuals who may not have the expertise to create such strategies on their own.

2. Long-Term Wealth Creation: By leveraging the power of compounding and strategic asset allocation, NPS aims to maximise wealth creation for retirement over the long term. The disciplined saving mechanism of NPS, coupled with prudent asset allocation, can potentially build a substantial retirement corpus.

3. Adaptability and Relevance: The adaptability of the NPS asset allocation options ensures that the system remains relevant across economic cycles and personal financial changes, making it a robust tool for retirement planning.

To sum up, the National Pension System’s asset allocation framework provides a strong foundation for retirement planning, embodying the principles of disciplined saving and investing. For Indian investors seeking a retirement solution that balances risk and reward while providing flexibility and control, NPS’s asset allocation strategies offer a compelling avenue. By aligning with general asset allocation principles and offering a mix of equities, corporate bonds, and government securities, NPS serves as an exemplar of how structured asset allocation can pave the way for long-term financial security.

Common Queries on Asset Allocation in the Indian Context

1. What is asset allocation and why is it important in India?

Asset allocation is the process of dividing investments across various asset classes like equities, debt, gold, and real estate to balance risk and return. In India’s volatile market, it’s crucial because it can help maximise returns while minimising risks, tailored to an individual’s financial goals and risk appetite.

2. How does my risk tolerance impact my ideal asset allocation in India?

Your risk tolerance dictates how much volatility you can handle in your investments. A high-risk tolerance may lead to a higher allocation in equities for growth, while low-risk tolerance may skew your portfolio towards bonds and fixed deposits for stability.

3. What are the main asset classes available in India for individual investors?

The main asset classes in India include equities (stocks), debt (bonds and fixed income securities), gold, real estate, and increasingly, alternative investments like mutual funds and ETFs.

4. What are the pros and cons of investing in equities, debt, gold, and real estate in India?

Equities offer high growth potential but come with high volatility. Debt offers stability and regular income with lower risk. Gold is a hedge against inflation but does not offer a regular income. Real estate can provide appreciation and rental income but requires high initial capital and has liquidity issues.

5. How do I choose appropriate mutual funds within each asset class for my portfolio in India?

Consider funds that align with your investment goals, risk tolerance, and time horizon. Look for a fund’s historical performance, management quality, expense ratios, and how it fits within your broader asset allocation strategy.

6. What is rebalancing and how often should I rebalance my portfolio in India?

Rebalancing is the process of realigning the weightings of a portfolio’s assets to maintain the original or desired level of asset allocation. In India, it’s generally advised to rebalance at least once a year or after significant market movements.

7. How do taxes affect my asset allocation decisions in India?

Taxes can significantly impact returns. Long-term capital gains tax on equity and debt investments, tax-free bonds, and tax implications on real estate sale and rent should be considered to optimize post-tax returns.

8. What are some common mistakes investors make with asset allocation in India?

Common mistakes include not diversifying enough, frequent trading, chasing past performance without a strategy, and not aligning investments with financial goals and risk profile.

9. Do I need a financial advisor to help me with asset allocation in India?

While not mandatory, a SEBI Registered Investment advisor can provide expert guidance tailored to your financial situation, help navigate India’s complex financial landscape, and assist in disciplined investing with regular portfolio reviews and rebalancing.

10. Where can I find reliable resources and tools for asset allocation in India?

Reliable resources include financial news platforms, SEBI’s official website, AMFI for mutual funds information, and various financial advisory services that offer asset allocation calculators and tools.

11. How should I adjust my asset allocation based on my age and life stage in India?

As a general rule, younger investors can allocate more to equities for long-term growth, while older investors nearing retirement should focus on capital preservation with a higher allocation to debt and fixed-income assets. Life-cycle funds can be a useful tool for automatic adjustments based on age.

Conclusion: Empowering Indian Investors Through Strategic Asset Allocation

Asset allocation, a cornerstone of effective financial planning, is pivotal in the diverse Indian investment landscape. It involves distributing investments across various asset classes like equities, debt, gold, and real estate to strike a balance between risk and return. The significance of asset allocation in India lies in its ability to cater to individual financial goals, risk appetites, and the dynamic nature of the Indian market.

Understanding and adapting to one’s risk tolerance is crucial in shaping the ideal asset allocation. Younger investors with a higher risk tolerance might incline towards equities for potential growth, while older investors generally prefer debt for stability. The Indian market offers a broad spectrum of asset classes, each with its unique set of pros and cons. Equities provide high growth potential but come with increased volatility, whereas debt offers stability with lower returns. Gold serves as a hedge against inflation, and real estate presents opportunities for capital appreciation and rental income, albeit with liquidity challenges.

Selecting appropriate mutual funds within each asset class requires consideration of personal investment goals, fund performance, and cost-efficiency. Regular portfolio rebalancing is essential to maintain the desired asset allocation, adapting to market shifts and personal financial changes. Tax considerations play a significant role in asset allocation decisions in India, influencing overall investment returns.

Common pitfalls in asset allocation include inadequate diversification, emotional trading, and misalignment with long-term objectives. Engaging a financial advisor can be beneficial for tailored advice and disciplined investment management. Reliable resources and tools for asset allocation are accessible through various online platforms, offering insights and calculators for informed decision-making.

As life stages and financial goals evolve, so should asset allocation. Young investors can benefit from an equity-heavy portfolio, gradually shifting to more conservative investments as they age. The National Pension System (NPS) in India exemplifies a structured approach to asset allocation, aligning with broader investment principles and offering flexibility across different life stages.

To sum up, asset allocation is an indispensable tool for Indian investors, essential for navigating the complexities of the market and achieving financial stability and growth. A well-considered asset allocation strategy, aligned with individual risk profiles and life stages, is key to realising long-term financial aspirations in the vibrant Indian economy.