Homeownership is a cherished dream for many, but the accompanying home loan often casts a long shadow on this achievement. The prospect of decades-long EMIs can be daunting. Yet, there exists a strategy akin to finding a hidden shortcut on a treasure map — home loan prepayment. This essential guide is your compass to navigate the waters of prepaying your mortgage, offering you the chance to claim early victory over your long-term financial obligations.

Every home loan has the core concepts of principal and interest, bound together by the thread of time. Comprehending this financial fabric is the first step towards unraveling the potential savings that early principal repayment can unfurl. In this article, we will dissect the anatomy of a home loan, laying bare the amortization process that dictates the ebb and flow of your repayment journey.

In the quest for financial liberation, prepayment options stand as beacons of hope. These are not mere monetary transactions but strategic maneuvers that can alter the course of your financial voyage, reducing the interest burden and shortening the journey’s duration. From part prepayments to lump sum injections, each action propels you further towards the haven of a debt-free life.

The act of prepayment is more than just a financial decision; it’s a liberation from future interest shackles. The psychological upliftment that accompanies the discharge of a debt can rekindle the joy of your home and open new doors for investment, allowing you to steer your resources towards uncharted opportunities for wealth accumulation. Sailing through the seas of home loan prepayment requires a keen understanding of the regulatory buoys and markers set by the RBI. This guide will serve as your navigational chart, clarifying the rules, demystifying the legal jargon, and ensuring you have all the necessary documents to plot a course towards successful prepayment.

With a prepayment calculator in hand, akin to a financial sextant, you will learn to gauge the treasure trove of savings awaiting discovery. By inputting variables such as interest rates and loan tenure, you will unveil the potential savings, illustrated through graphs that make understanding your financial horizon straightforward. However, not all voyages are meant for every traveler. The decision to embark on the prepayment journey must be weighed against your financial situation, considering whether it harmonizes with your personal wealth-building symphony. This guide will offer perspectives to help you assess if prepayment aligns with your financial objectives.

Tax implications are often a maze of complexity. Our guide will serve as your map, helping you navigate the tax relief terrain that accompanies home loan prepayment, ensuring you emerge with the maximum fiscal advantage. Just like every mariner faces storms; similarly, homeowners contemplating prepayment may encounter doubts and obstacles. We will tackle these challenges head-on, equipping you with the strategies to remain steadfast in your prepayment course.

This article is your invitation to embark on a transformative financial journey. As you read on, envision a future where you stand on the deck of your home, no longer weighed down by the anchor of a home loan, with the flag of financial freedom proudly hoisted high.

Understanding Home Loan Principal Repayment

A home loan is more than just a pathway to homeownership; it’s a financial instrument that binds you with a promise to repay the sum borrowed alongside the cost it carries — the interest. This sum, known as the principal, is the core of your loan agreement, the very essence of what you sought to borrow to turn your dream home into a reality.

EMIs – Monthly Payments

With each EMI, you’re not just inching closer to fully owning your abode but also fulfilling a dual commitment. A slice of your payment diminishes the principal, slowly chipping away at the mountain of the borrowed sum, while another portion goes towards the interest, the price of the financial leverage granted to you.

Amortization Schedules

Amortization schedules serve as lighthouses, guiding you through the foggy complexity of loan repayment. They lay out a roadmap of how your repayment journey will progress — how each EMI contributes to reducing the principal and how much it appeases the interest. This clarity is vital as it unveils the potential savings that could be harnessed by repaying the principal ahead of schedule.

Mastering the Repayment Strategy

Understanding your amortization schedule empowers you to strategize. You can plan additional payments that directly target the principal, thus lowering the overall interest that would accumulate in the years to come. This is a strategy often echoed by SEBI Registered Investment advisors, who recognize the substantial long-term savings it can yield.

The Wisdom in Early Principal Repayment

There’s a sage financial wisdom in choosing to repay the principal early. It’s akin to planting a tree; initially, the growth is slow, but over time, you reap the benefits manifold. Similarly, each additional payment towards the principal is like nurturing the roots of your financial tree, ensuring it stands strong and saves you a considerable sum in future interest payments.

The Echoing Advice of Financial Experts

The consensus among financial experts is clear — prioritize early principal repayment. This approach is akin to finding a shortcut on a long trail; it can significantly cut down the journey’s length and lead to substantial savings on the interest front. It’s a simple yet effective technique that can make a profound difference in your financial well-being over the loan’s tenure.

The Advantage of Early Repayment

Early repayment is not just about savings; it’s about financial freedom. By reducing the principal earlier in the loan’s life, you’re setting the stage for a future where your income isn’t tied up in debt repayment, freeing up funds for other areas of wealth management and investment. It’s a strategic move that aligns with the principles of liquidity, safety, and growth — the pillars of the LSG framework that forms the bedrock of prudent financial planning and wealth management.

Grasping the concept of home loan principal repayment is the key to unlocking the door to potentially significant interest savings. It’s a disciplined approach that, when paired with a comprehensive understanding of your amortization schedule, can accelerate your journey to financial freedom, allowing you to grow your wealth and explore new investment horizons with the guidance of a trusted SEBI Registered Investment advisor.

Strategising Your Home Loan Prepayment Options

When you opt for part prepayment, it’s like paying an advance on your future, allowing you to contribute more than your scheduled EMI. This act is a stroke of financial prudence, enabling you to whittle down the outstanding loan balance and, subsequently, the interest that accrues over the years. Part prepayment stands out for its flexibility; it’s a financial lever you can pull without stretching your finances too thin, making it a viable option for many homeowners.

The Transformative Potential of Lump Sum Payments

Consider the lump sum payment as a financial masterstroke. By channeling surplus funds into your home loan, you can dramatically diminish the principal, thereby recalibrating both the interest component and the remaining tenure of your loan. It’s a powerful strategy that can alter the trajectory of your repayment schedule. However, it’s essential to navigate this path with caution, ensuring that your emergency funds remain intact and your liquidity needs are met.

Tailoring Your Loan with Prepayment

Prepayment offers a tailor-made approach to managing your home loan. It’s akin to adjusting the sails of your financial ship to catch the winds of economic advantage. By prepaying, you earn the latitude to either lighten the monthly load by reducing your EMI or shorten the voyage by cutting down the loan tenure. The former can free up monthly cash flow for other investments, while the latter can culminate in long-term interest savings, underlining the importance of strategic financial planning in wealth management.

In essence, home loan prepayment options furnish you with the tools to sculpt your financial future and enhance your wealth management strategy. They empower you to reduce your interest burden or expedite your journey to becoming debt-free. With guidance from a SEBI Registered Investment advisor, you can discern the right prepayment plan that harmonizes with your financial goals, ensuring that each step you take is a measured stride towards financial liberation and growth.

Benefits of Home Loan Prepayment

The decision to prepay your home loan is akin to planting a seed that yields savings for years to come. By choosing to reduce your principal earlier, you’re effectively pruning the interest that would otherwise compound, burdening your future finances. It’s a strategic move that enhances the cost-efficiency of your loan, allowing you to revel in the savings generated over the loan’s lifespan. The mantra is simple: the sooner you prepay, the more you save, making it an intelligent move in the chess game of financial planning.

The Bliss of a Debt-Free Existence

Imagine lifting the veil of debt from your life’s canvas much earlier than predicted. Prepaying your home loan paves the way for this reality, offering you not just a clear conscience but a realm of financial flexibility. It is about transcending the norm of living with debt to a space where your income is yours to command—be it channeling funds into investments, retirement planning, or indulging in the joys and experiences life has to offer, unbridled by the chains of ongoing debt.

Drawing Inspiration from Real-life Victories

Just as a seasoned gardener learns from the successes of fellow enthusiasts, homeowners can draw valuable lessons from others who have navigated the path of home loan prepayment. The narratives of those who have successfully managed to prepay their home loans are not just heartening but are a treasure trove of insights. They shine a light on the tangible impact of prepayment, offering a blueprint for achieving financial success and serving as a beacon for others to follow.

The benefits of home loan prepayment are manifold, encompassing both financial gains and personal well-being. They affirm the wisdom in proactive financial management and are a testament to the power of taking control of one’s financial destiny. With the expertise of a SEBI Registered Investment advisor, you can navigate this path effectively, ensuring that your journey toward financial freedom is both strategic and rewarding.

Rules and Regulations for Home Loan Prepayment

Understanding the regulatory and legal framework governing home loan prepayment is crucial for homeowners. It’s like deciphering a map that leads to financial liberation. The Reserve Bank of India (RBI), as the custodian of financial regulation, has laid down guidelines that streamline and facilitate the prepayment process, ensuring a fair and transparent journey for borrowers.

The RBI’s Role in Simplifying Prepayment

The RBI’s regulations are designed to ease the prepayment process, removing hurdles that previously deterred borrowers from considering this option. By standardizing practices across financial institutions, the RBI ensures that your right to prepay your loan is both accessible and straightforward.

These guidelines are not just rules; they’re a protective shield for your financial interests. They prevent undue exploitation and ensure that the process is aligned with fair banking practices, safeguarding you from hidden charges or exploitative terms.

Understanding Your Loan Agreement

Your loan agreement is a treasure trove of information. Paying close attention to the clauses related to foreclosure and part prepayment is akin to studying the key details of a financial contract. These clauses will outline the terms of prepayment, any fees involved, and the procedural nuances, providing clarity and direction for your prepayment strategy.

Each home loan is unique, and so are its terms and conditions. Familiarizing yourself with these specifics will empower you to make informed decisions, ensuring that your prepayment journey is aligned with your financial goals and circumstances.

Legalities and Documentation

Prepayment is not just a financial transaction; it’s a legal process that requires due diligence. Ensuring that you have all the necessary documentation in place is critical for a smooth transition. It’s about crossing the t’s and dotting the i’s, making sure every legal aspect is addressed.

The paperwork involved in prepayment can be extensive, ranging from prepayment notices to revised amortization schedules. Having these documents in order ensures that your prepayment is not just effective but also legally sound.

Navigating the legalities of home loan prepayment can be daunting. Consulting with a SEBI Registered Investment advisor or a legal expert can provide clarity and direction, ensuring that your journey towards prepayment is free from legal hurdles.

Understanding the rules and regulations set forth by the RBI, comprehending the clauses in your loan agreement, and ensuring that all legal aspects of prepayment are addressed are key steps in your journey towards home loan prepayment. With the right guidance and a clear understanding of the legal landscape, your path to prepaying your home loan can be a smooth and rewarding journey, aligning perfectly with your broader wealth management strategy.

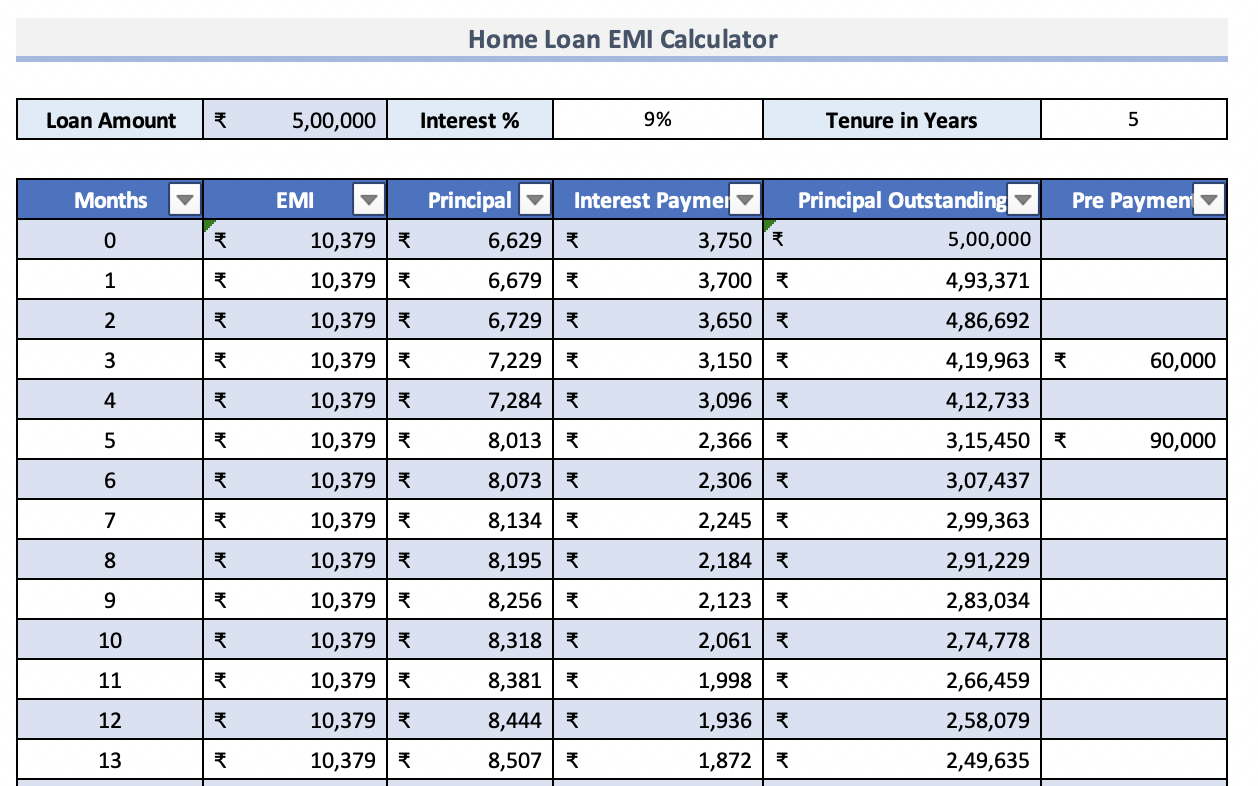

Calculating Savings from Prepayment

Prepaying a home loan is a strategic maneuver, a decision that can lead to significant savings over time. To navigate this financial journey effectively, harnessing the capabilities of prepayment calculators is essential. These tools are not just calculators; they are financial compasses that guide you towards making informed decisions about your home loan.

The Power of Prepayment Calculators

Prepayment calculators are akin to time machines; they give you a glimpse into the future of your loan’s trajectory post-prepayment. By inputting details such as your loan’s interest rate, tenure, and the principal amount, these calculators provide you with precise projections of the savings you can accrue by prepaying your home loan.

Every home loan is unique, and so are the savings from prepayment. These calculators tailor their output to your loan’s specifics, offering a customized view of how prepayment can reshape your financial landscape. This personalized projection is crucial in planning your finances effectively, ensuring that your decision to prepay is grounded in solid data.

Deciphering the Variables Impacting Savings

The interest rate on your loan is the linchpin in the calculus of prepayment. Higher interest rates generally translate to greater savings through prepayment, as each rupee prepaid saves more in future interest.

The duration of your loan also plays a crucial role. Prepaying early in the loan tenure can lead to more significant savings, as it reduces the principal amount on which future interest accrues. The size of your loan determines the potential for savings. Larger loans offer a wider canvas for savings through prepayment, making it an attractive option for borrowers with substantial loan amounts.

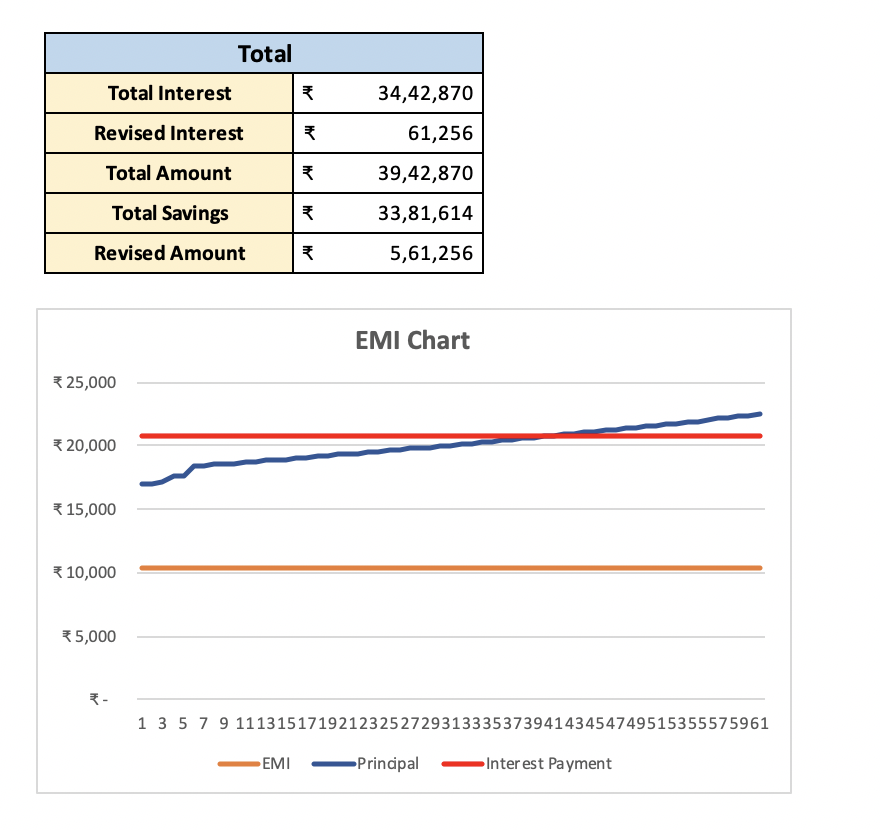

Visualizing Your Financial Future

The benefits of prepayment, while significant, can sometimes be abstract and hard to grasp. This is where visual aids come in. Graphs and charts break down the impact of prepayment in an easily digestible format, illustrating how your loan balance and interest obligations diminish over time with prepayment. These visual representations paint a clear picture of your financial journey post-prepayment. They show the gradual reduction in your loan balance and the corresponding decrease in interest payments, helping you visualize the journey to becoming debt-free.

Graphs and visual aids are not just tools for understanding; they are educational resources that empower you to make informed decisions. By visually articulating the impact of prepayment, they demystify the financial implications, making the concept accessible even to those new to the nuances of home loan management.

Calculating the savings from home loan prepayment, aided by calculators and visual tools, is an essential step in your financial journey. It’s a step that not only illuminates the path to savings but also empowers you with the knowledge to make decisions that align with your long-term financial goals. This calculative approach, coupled with expert advice from a SEBI Registered Investment advisor, can ensure that your journey towards a debt-free life is not just a dream, but a well-charted plan set firmly in reality.

Is Home Loan Prepayment a Good Option?

The question of whether to prepay your home loan is like standing at a financial crossroads. The path you choose must align with your broader financial landscape and long-term objectives. Home loan prepayment can be a powerful strategy for wealth management, but it necessitates a thorough evaluation of your personal financial situation and goals.

Tailoring Decisions to Personal Financial Objectives

Like a tailor crafting a bespoke suit, the decision to prepay your home loan must be custom-fitted to your financial profile. This involves assessing your current financial health, future income prospects, and existing financial obligations. It’s about understanding where you stand today and where you aim to be in the future.

Your financial goals are unique to you. For some, the peace of mind that comes with being debt-free is paramount, while for others, maximizing wealth through diverse investments takes precedence. It’s essential to introspect and prioritize what matters most to you in your financial journey.

Expert Perspectives on Prepayment

Financial experts often tout the virtues of prepaying a home loan, primarily due to the long-term savings on interest payments. However, these advisors also emphasize the significance of timing. The ideal moment for prepayment is when it seamlessly fits into your financial plan without disrupting your other fiscal responsibilities and goals.

The decision to prepay should be a well-timed move, considering factors like your cash flow, emergency funds, and upcoming financial needs. The benefits of prepayment extend beyond interest savings; it’s about gaining financial freedom and redirecting your resources towards achieving other financial milestones.

Balancing Prepayment with Other Investment Opportunities

When contemplating prepayment, it’s crucial to weigh the opportunity cost. This involves comparing the guaranteed savings from prepayment against potential returns from other investment avenues. It’s a financial balancing act where you must consider the returns you could garner by investing the prepayment amount in other wealth-generating opportunities.

While the allure of higher returns from investments like equities or mutual funds is undeniable, these come with inherent risks. On the other hand, prepaying your home loan offers a guaranteed return in the form of interest savings. Deciding between these options requires a thorough evaluation of your risk tolerance, investment horizon, and financial stability.

If your investment portfolio is already well-diversified and aligned with the Roots and Wings investment philosophy – emphasizing both stability and growth – prepaying your home loan might make more financial sense. However, if there are gaps in your portfolio that offer potentially higher returns, allocating funds to these investments could be more beneficial.

The decision to prepay your home loan is multifaceted and must be made after a comprehensive analysis of your financial goals, investment opportunities, and personal circumstances. It’s a decision that should align with your overall wealth management strategy, ensuring that each financial move you make is a step towards achieving your long-term objectives. As always, consulting with a SEBI Registered Investment advisor can provide valuable insights and guidance, helping you navigate this decision with expertise and confidence.

Tax Implications of Home Loan Prepayment

The decision to prepay your home loan, a significant milestone in your financial journey, can have notable tax implications. Understanding these implications is akin to unraveling a complex puzzle, one that requires both knowledge and strategy. In the realm of wealth management, it’s not just about paying off debt early; it’s about doing so in a way that maximizes your fiscal advantages under the Income Tax Act.

The Interplay of Prepayment and Tax Benefits

Home loan repayments come with the perk of tax deductions under various sections of the Income Tax Act. However, prepaying your loan changes this equation. As you reduce your loan principal through prepayment, the interest component – which offers tax relief – also diminishes. This calls for a careful assessment of how prepayment impacts your tax-saving strategy.

The art of managing your finances lies in striking a balance between reducing your debt and optimizing tax benefits. While prepayment leads to interest savings, it’s essential to measure this against the tax deductions you might lose as a result. The key is to weigh the immediate financial relief against the long-term tax savings.

Optimizing Tax Strategy Around Prepayment

Navigating the tax implications of prepayment requires a calculated approach. It’s not just about paying off your loan early; it’s about understanding how this decision fits into your broader tax planning strategy. For instance, if the tax benefits outweigh the interest savings, it might be more prudent to continue with regular repayments.

This is where the expertise of a SEBI Registered Investment advisor becomes invaluable. They can provide insights into the nuances of tax planning around home loan prepayment, helping you craft a strategy that aligns with your overall financial goals.

A SEBI Registered Investment advisor can guide you through the labyrinth of tax laws and regulations. Their advice can help you understand the optimal point of prepayment – where you maximize both interest savings and tax benefits. This kind of professional guidance is crucial in making an informed decision that aligns with your financial aspirations.

The Impact of Prepayment on Deduction Claims

Once you prepay your home loan, the landscape of your tax deductions changes. It’s important to reassess your eligibility for claiming deductions post-prepayment and adjust your tax filings accordingly. This reassessment ensures you’re not missing out on any fiscal benefits you’re entitled to.

As you reduce your loan liability through prepayment, the amount eligible for tax deductions under sections like 80C (for principal repayment) and 24b (for interest payment) also changes. Being aware of this shift is crucial for effective tax planning.

The tax implications of home loan prepayment are a critical component of your financial planning process. By understanding how prepayment affects your tax benefits and strategically planning around it, you can ensure that your journey to becoming debt-free is not only financially rewarding but also tax-efficient.

Overcoming Challenges in Home Loan Prepayment

Home loan prepayment, while a strategic move towards financial freedom, often comes with its set of challenges and concerns. Addressing these obstacles is not just about having the means; it’s about having a plan and the discipline to follow it through. For homeowners, navigating this path requires a blend of financial acumen, adaptability, and resilience.

Addressing Common Prepayment Concerns

The journey of prepaying a home loan is often shrouded in myths and misunderstandings. Common concerns range from fears about liquidity to misconceptions about the benefits of prepayment. Dispelling these myths is essential. It involves understanding that prepayment can lead to substantial interest savings and can be a feasible option even if it means making small, additional payments over time.

A successful prepayment strategy requires more than just the desire to pay off the loan early; it requires a practical and well-thought-out plan. This might involve reassessing your monthly budget, cutting down on non-essential expenses, or even considering alternate sources of income to free up funds for prepayment.

Navigating Financial Challenges in Prepayment

Financial journeys are rarely linear; they’re filled with ups and downs. Encountering financial setbacks shouldn’t deter you from your prepayment goals. It’s about being flexible and adapting your prepayment plan to your changing financial circumstances, ensuring that you continue making progress, however incremental it may be.

While being aggressive in loan prepayment can be tempting, it’s crucial to balance this with maintaining a safety net for emergencies. This means ensuring that your prepayment plan doesn’t compromise your overall financial security and liquidity.

Cultivating the Discipline for Prepayment

Discipline in prepayment starts with setting clear financial priorities. It involves distinguishing between ‘wants’ and ‘needs’ and aligning your spending with your long-term goal of loan prepayment.

One effective way to maintain discipline is by automating a portion of your income towards prepayment. This could mean setting up automatic transfers to a dedicated prepayment fund as soon as your salary is credited. Automation helps in maintaining consistency in savings, making prepayment a part of your financial routine.

Keeping your eyes on the prize is crucial. Reminding yourself of the benefits of prepayment, such as interest savings and the peace of being debt-free, can keep you motivated. Regularly reviewing your loan balance and the progress you’ve made can also serve as a motivating factor.

Overcoming the challenges in home loan prepayment requires a mix of practical strategies, adaptability to financial situations, and unwavering discipline. Each step taken towards prepayment is a step towards financial liberation and should be aligned with your overall wealth management strategy. With patience and perseverance, the goal of a debt-free life is well within reach.

FAQs on Home Loan Prepayment

Home loan prepayment raises numerous questions for homeowners. Here are some answers to the most common queries:

Can I Prepay a Fixed-Rate Home Loan?

Yes, you can prepay a fixed-rate home loan, but it might involve a prepayment penalty depending on the terms set by the lender.

Home Loan Prepayment and Credit Score Impact

Prepaying a home loan can positively impact your credit score by lowering your debt-to-income ratio. However, ensure timely payments to maintain a good credit history.

Post-Prepayment EMI Schedule

After prepayment, you can either reduce the EMI amount or the loan tenure, depending on your financial goals and lender’s terms.

Eligibility Criteria for Home Loan Prepayment

Generally, there are no specific eligibility criteria for prepayment, but lenders may have terms regarding the minimum amount or the number of times you can prepay.

Negotiating Favorable Prepayment Terms

It’s possible to negotiate with banks for favorable prepayment terms. Being informed about your lender’s policies and maintaining a good repayment record can aid in negotiation.

Financial Difficulties After Prepayment

If you face financial challenges after making a prepayment, it’s crucial to have an emergency fund or to explore options like loan restructuring.

Joint Home Loan and Independent Prepayments

Joint home loan holders can independently make prepayments. However, both parties should agree on the terms to avoid future disagreements.

To sum up, home loan prepayment is a strategic financial move that can lead to substantial savings and peace of mind. It’s a decision that should be weighed against other investment opportunities, tax implications, and your financial readiness. Like the careful pruning of a bonsai, it requires a delicate balance between aggressive debt reduction and nurturing other areas of your financial garden.

Practical steps you can take right away include reviewing your loan details, using prepayment calculators, and consulting with a SEBI Registered Investment advisor. Remember, every step towards prepaying your home loan is a step towards financial freedom and a secure, prosperous future. If you seek guidance on this journey, consider the expertise of Jama Wealth’s PMS services and their investment advisory, tailored to ensure your financial strategies are as sound as they are rewarding.