The National Pension Scheme (NPS) is one of the prominent investment avenues in India’s retirement planning landscape. Introduced by the Indian government, its primary objective is to provide a stable and continuing source of income to individuals post-retirement, ensuring financial security and independence. NPS, a voluntary, long-term investment plan, is designed to cater to the retirement needs of every Indian citizen, fostering a culture of savings and investment among the working population.

Launched in January 2004 initially for new government recruits (excluding armed forces), the NPS was expanded to include all citizens on a voluntary basis in 2009. This evolutionary leap was aimed at filling the gaping void in the retirement planning domain, offering a structured and regulated pension scheme that could effectively bridge the pension divide across various sectors. Over the years, NPS has undergone numerous refinements, enhancing its appeal and accessibility, making it a cornerstone of retirement planning for millions of Indians.

Understanding the Structure of NPS

Overview of Tier I and Tier II Accounts

NPS is structured around two account types: Tier I and Tier II. The Tier I account is mandatory for all enrollees, serving as the primary pension account with restrictions on withdrawals to ensure the funds are preserved for retirement purposes. On the other hand, the Tier II account is optional and more flexible, allowing for withdrawals at the account holder’s discretion, making it akin to a savings account but with the benefit of long-term investment.

Key Features and Benefits

NPS is lauded for its flexibility, portability, and the wide array of investment options it offers. Subscribers can choose between different asset classes, and adjust their portfolio according to their risk appetite and financial goals. The scheme’s transparency and low-cost structure further enhance its attractiveness, providing subscribers with detailed information about their investments and ensuring that more of their money is working for them.

Eligibility and Registration Process for NPS

The NPS is accessible to all Indian citizens between the ages of 18 and 65, catering to a broad demographic spectrum. This inclusivity reflects the scheme’s aim to provide a universal retirement solution, bridging the gap between various employment sectors and demographic segments.

Registering for the National Pension Scheme has been designed to be an inclusive and straightforward process, ensuring wide accessibility across India’s diverse demographic. Whether you’re tech-savvy or prefer the traditional touch, NPS registration accommodates all preferences. Here’s a detailed guide to navigating this essential step towards securing your financial future:

Step-by-Step Guide to Registering for NPS

Step 1: Choose Your Registration Mode

– Online through e-NPS: Ideal for those comfortable with digital platforms, offering a quick and paperless registration process.

– Offline through Points of Presence (PoPs): Suitable for individuals who prefer face-to-face interactions or require assistance during the registration process. PoPs include banks, financial institutions, and designated service providers spread across the country.

Step 2: Gather Required Documents

– Identity Proof: Aadhar Card, PAN Card, Voter ID, or Passport.

– Address Proof: Recent utility bills, bank statements, Aadhar Card, or Passport.

– Age Proof: Birth certificate, SSLC Book/Certificate, Passport.

– A Passport-sized Photograph.

Step 3: Filling the Application

– Online: Visit the e-NPS portal (https://enps.nsdl.com), select ‘National Pension System’ and choose ‘Registration.’ Fill in the required details, upload scanned copies of your documents, and proceed to make your initial contribution through net banking, debit/credit card, or UPI.

– Offline: Visit your nearest PoP, collect the NPS registration form (Form CSRF), fill it out accurately, attach photocopies of your documents, and submit it alongside your photograph and initial contribution.

Step 4: Making the Initial Contribution

– The minimum initial contribution to activate an NPS account is ₹500 for Tier I and ₹1,000 for Tier II accounts. This contribution can be made online for e-NPS registrants or via cheque/cash at the PoP for offline applicants.

Step 5: PRAN Generation and Kit Receipt

– Once your application and initial contribution are processed, you will be allotted a Permanent Retirement Account Number (PRAN), a unique identifier for your NPS account.

– Online applicants will receive an electronic PRAN card and welcome kit via email.

– Offline applicants will receive a physical PRAN card and welcome kit through post or can collect it from the PoP.

Step 6: Activating e-NPS Services (for Offline Registrants)

– If you registered offline and wish to manage your account online, visit the e-NPS portal, use the ‘Activate Tier II account’ or ‘eSign’ options to digitise your account management. This step requires verification through an OTP sent to your registered mobile number linked with Aadhar.

Step 7: Nominee Addition and Investment Choice

– Subsequently, you can log into your NPS account using your PRAN and password to add nominees and select your investment choices and pension fund manager. You can opt between ‘Active Choice’ (self-managing asset allocation) or ‘Auto Choice’ (automated asset allocation based on age).

Step 8: Continuous Contribution and Account Management

– With your NPS account now active, you can continue making contributions, adjusting your investment choices, and tracking your portfolio performance through the e-NPS portal or by visiting your PoP.

This comprehensive process underscores the NPS’s commitment to providing a seamless and user-friendly path to retirement savings. With options catering to all Indians, the NPS ensures that preparing for retirement is a convenient and accessible endeavour.

National Pension Scheme Trust and NSDL

NSDL (National Securities Depository Limited) plays a crucial role in the National Pension System. As the central recordkeeping agency for NPS, NSDL is the backbone ensuring the operational efficiency, security, and transparency of the system. With its advanced technological framework and robust infrastructure, NSDL facilitates the meticulous management of millions of NPS accounts, enabling seamless transactions, accurate record maintenance, and reliable customer service.

This partnership exemplifies the successful integration of technology in the financial sector, offering a secure and user-friendly platform for subscribers to plan their retirement. The collaboration between NSDL and the NPS brings a modern approach to traditional pension schemes, reflecting the evolving landscape of India’s financial services sector.

By providing a digital-first experience, NSDL empowers individuals across the country to take control of their retirement savings, ensuring a smooth transition from active employment to retirement. Through its commitment to excellence and innovation, NSDL has significantly contributed to the growth and success of the NPS, making retirement planning accessible and straightforward for the Indian populace.

NPS Contribution and Investment Options

National Pension Scheme offers an avenue for subscribers to craft a retirement savings strategy that aligns seamlessly with their financial landscape and long-term aspirations. The scheme’s flexible contribution framework coupled with a broad spectrum of investment options provides a foundation for personalised financial planning.

Flexible Contribution Schedules

At the heart of NPS’s design is the principle of adaptability, allowing subscribers to set the cadence and volume of their investments. The scheme mandates a minimum annual contribution of ₹1,000 for Tier I accounts, ensuring the account remains active while affording subscribers the latitude to increase their contributions as their financial situation permits. This flexibility is pivotal, especially in catering to the diverse economic backgrounds of its vast subscriber base, enabling everyone from young professionals to seasoned businesspersons to participate in and benefit from the scheme.

Tailoring Contributions to Financial Goals

Subscribers are encouraged to periodically review and potentially adjust their contributions based on life changes, financial milestones, or shifts in income. This dynamic approach empowers individuals to synchronise their NPS contributions with their evolving financial landscape, optimising their retirement savings to achieve specific future financial goals.

Customizable Asset Allocation

The NPS stands out for its diverse investment avenues, spanning equities, corporate bonds, government securities, and alternative assets. This multifaceted investment palette not only diversifies risk but also amplifies the potential for growth, mirroring the complexity and vibrancy of India’s own financial market.

Active and Auto Choices

For those with a keen interest in the markets or specific financial strategies, the Active Choice option serves as a canvas, offering the freedom to sculpt their fund allocations across different asset classes. This hands-on approach suits subscribers who wish to fine-tune their investment strategies based on market performance or their risk appetite.

Conversely, the Auto Choice simplifies asset allocation, making it accessible for novices or those preferring a hands-off approach. Based on a lifecycle fund model, this option automatically rebalances the asset mix as the subscriber ages, gradually transitioning from equity-heavy investments towards more conservative assets. This automated recalibration ensures the investment strategy remains aligned with decreasing risk tolerance as retirement approaches, embodying a prudent approach to long-term savings.

The integration of flexible contributions and diversified investment choices under the NPS framework underscores its role as a cornerstone in the retirement planning process. It encourages a proactive, informed approach to retirement savings, urging subscribers to engage with their investments actively. Whether through selecting specific asset classes in the Active Choice or relying on the age-adjusted Auto Choice model, NPS provides a structured yet flexible path towards achieving financial security in retirement.

In essence, the National Pension Scheme’s contribution and investment frameworks are meticulously designed to accommodate the nuances of individual financial journeys. They reflect a deep understanding of the varied needs and aspirations of its subscribers, offering a robust platform for building a secure, growth-oriented retirement corpus.

Tax Benefits of National Pension Scheme

Understanding the tax implications of any retirement savings product is crucial for maximising financial security in your later years. The National Pension Scheme, with its advantageous tax treatment, stands out as a compelling choice for individuals seeking to enhance their retirement savings with tax efficiency in mind. Here’s an in-depth look at the tax benefits associated with NPS contributions, withdrawals, and maturity.

Tax Exemption on NPS Contributions

One of the most significant advantages of investing in NPS is the attractive tax exemption on contributions, which serves as a dual incentive – promoting retirement savings while offering immediate tax relief. Under Section 80C of the Income Tax Act, subscribers can claim a deduction for their contributions to the NPS (up to ₹1.5 lakh per annum), which is part of the overall limit of this section. Moreover, NPS subscribers get an exclusive additional deduction under Section 80CCD (1B), allowing for an additional deduction of up to ₹50,000, which is over and above the ₹1.5 lakh limit under Section 80C. This unique tax advantage makes NPS an attractive vehicle for tax-saving and retirement planning.

Enhanced Tax Benefits for Employers and Employees

It’s also worth noting that contributions made by an employer towards an employee’s NPS account are deductible under Section 80CCD(2), with no upper limit. This particular benefit is exclusive to NPS and does not impact the ₹1.5 lakh ceiling under Section 80C, making it an efficient tax-saving tool for both employers and employees.

Tax Treatment on Withdrawals and Maturity

The NPS also extends its tax-friendly nature to withdrawals and maturity, adhering to guidelines that balance immediate financial relief with long-term savings incentives. At the time of retirement or upon reaching the age of 60, subscribers can withdraw up to 60% of the corpus tax-free. The remaining 40% must be mandatorily used to purchase an annuity, which is also tax-exempt. This provision ensures that a significant portion of the retirement savings can be accessed without tax liability, while also ensuring a steady income stream through the annuity.

For partial withdrawals, which are allowed under specific conditions like education, marriage, or the purchase/construction of a primary residence, subscribers can withdraw up to 25% of their contributions tax-free, provided they have been part of the scheme for at least three years. These conditions underscore the scheme’s design to serve not only as a retirement fund but also as a support during critical financial needs before retirement.

Leveraging NPS for Tax-Efficient Retirement Planning

The tax benefits offered by NPS make it an integral component of a comprehensive retirement planning strategy. By utilising the full extent of tax deductions available under Sections 80C and 80CCD, subscribers can significantly reduce their taxable income each year, while simultaneously building a sizable retirement corpus. Moreover, the tax-exempt nature of a large part of the withdrawal amount at maturity further enhances the appeal of NPS as a retirement savings vehicle.

National Pension Scheme Interest Rates and Returns

The National Pension Scheme stands as a lighthouse for those navigating the sometimes turbulent waters of retirement planning in India. Unlike the static returns of traditional fixed deposits, the NPS rides the waves of market fluctuations, offering returns that reflect the performance of its diversified asset classes: equity, government securities, corporate bonds, and alternative investments.

Understanding the Interest Rate Dynamics

Embarking on an NPS investment journey is akin to embracing the varied climatic zones of India—from the crisp air of the Himalayas to the balmy breezes of the coastal regions. The returns on NPS investments do not follow a linear path; they are influenced by a complex interplay of global economic trends and domestic fiscal policies. This inherent variability highlights the scheme’s dynamic nature, urging investors to look beyond static interest rates and consider the broader horizon of growth potential.

The performance of NPS funds, much like the weather, is subject to change, influenced by the economic environment, policy decisions, and market movements. Understanding these dynamics is crucial for setting realistic expectations and crafting a strategy that aligns with one’s financial goals and risk tolerance.

Expected Returns and Growth Potential

The spectrum of NPS investment choices spans from conservative to aggressive, mirroring the diverse investment appetites across India’s demographic landscape. The scheme’s flexibility allows subscribers to tailor their portfolios according to their risk profiles, with the potential for higher returns accompanying higher risk levels.

Historically, the NPS has demonstrated its capacity to generate competitive returns, often surpassing those offered by traditional retirement saving avenues. This performance is not just a reflection of market conditions but also the skill and strategy of fund managers who deftly navigate the investment terrain. The National Pension Scheme offers a range of investment schemes tailored to match different risk appetites and financial goals.

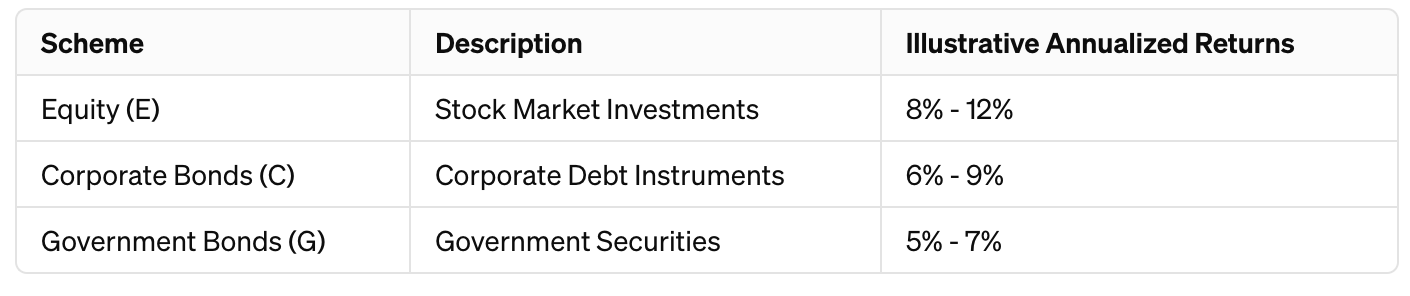

Among these, the three primary schemes are Equity (E), Corporate Bonds (C), and Government Bonds (G). The Equity scheme allows for higher growth potential through investments in stock markets, suitable for those willing to accept higher volatility for the possibility of greater returns. Corporate Bonds offer a balance between risk and return, focusing on debt instruments issued by companies, while Government Bonds are the most conservative option, investing in secure government securities.

Illustrative returns across these schemes vary based on market conditions, the economic environment, and the investment horizon. Below is a table showcasing hypothetical annualised returns for each scheme, emphasising the diversification and potential growth NPS offers:

These returns are illustrative and can fluctuate based on market dynamics. The NPS allows subscribers to mix and match these schemes according to their risk tolerance and investment goals, providing a customised approach to retirement planning. The real growth story of NPS, however, is one of patience and long-term commitment. It is based on the core principles of compounding interest and strategic asset allocation. Subscribers who stay the course, allowing their investments to mature over decades, are often rewarded with substantial growth, echoing the upward trajectory of India’s own economic development.

Navigating NPS for Optimal Returns

Investing in NPS requires a mindset geared towards the long haul, emphasising steady growth over immediate gains. The choice of asset allocation plays a pivotal role in determining the overall returns. Those opting for a higher allocation to equities may see more significant fluctuations in their fund value but also have the potential for higher returns in the long term. Conversely, a conservative strategy focusing on government securities and corporate bonds offers stability but may yield lower returns.

Subscribers must also consider the impact of external factors such as inflation and changing interest rates on their retirement savings. A well-considered NPS portfolio, diversified across asset classes, can serve as a bulwark against these uncertainties, ensuring a balance between risk and return.

NPS Withdrawal Rules and Options

The National Pension Scheme strikes a fine balance between rigidity and adaptability, designed to secure financial stability for the golden years while accommodating the unpredictable nature of life’s financial demands. The scheme differentiates between two types of accounts, Tier I and Tier II, each with its distinct withdrawal rules, underscoring the scheme’s dual objectives of fostering disciplined long-term savings and providing liquidity when needed.

Guidelines for Withdrawals from Tier I and Tier II Accounts

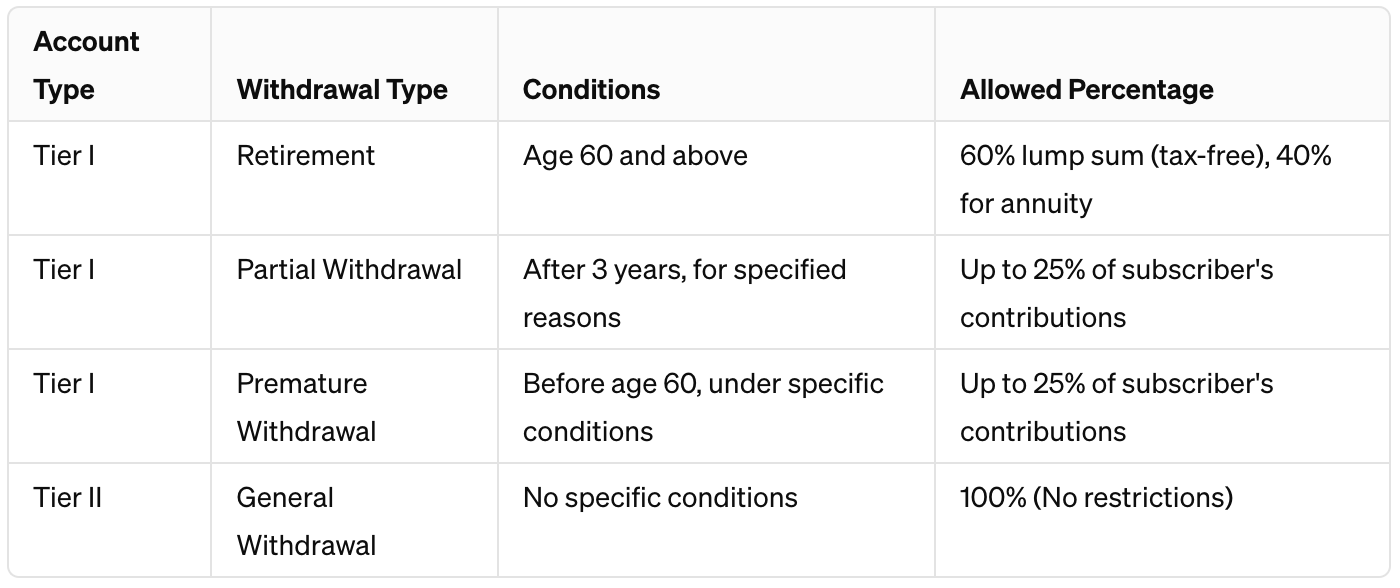

Tier I accounts form the backbone of the NPS, primarily focused on retirement savings. Withdrawals from these accounts are tightly regulated to preserve the corpus for the subscriber’s retirement. Generally, withdrawals are allowed only upon reaching the age of 60, with the scheme permitting up to 60% of the corpus to be withdrawn tax-free, while the remaining 40% must be utilised to purchase an annuity, ensuring a steady income stream post-retirement.

In contrast, Tier II accounts offer a more flexible savings solution, acting as an accessible fund for subscribers’ short-term financial needs. Unlike Tier I, there are no restrictions on withdrawals from Tier II accounts, making it an attractive option for investors seeking both growth and liquidity from their investments.

Flexibility and Conditions for Partial and Premature Withdrawals

NPS is attuned to the life’s unforeseen financial exigencies, offering provisions for partial withdrawals from Tier I accounts. Subscribers can withdraw up to 25% of their contributions (excluding employer’s contribution) for specific purposes such as higher education of children, marriage, and medical treatment for family members. These withdrawals can be made after three years of subscription to the scheme, emphasising the scheme’s flexibility within a framework designed to protect the retirement corpus.

For those needing to access their funds before reaching the age of 60, NPS permits premature withdrawals under certain conditions, but with a cap of 25% of the subscriber’s contributions. This feature is particularly beneficial for meeting unexpected financial needs without derailing retirement savings goals.

An Illustration of Withdrawal Options

To visualise the NPS withdrawal rules, consider the following table which simplifies the guidelines:

This structure illustrates the NPS’s thoughtful approach, designed to cater to both the long-term goal of securing a financially stable retirement and addressing immediate financial needs through the Tier II account. The scheme’s withdrawal rules are emblematic of a well-thought-out structure that supports disciplined savings while recognizing the necessity for financial flexibility. By delineating clear guidelines for withdrawals from Tier I and Tier II accounts, the NPS ensures subscribers have a robust framework for retirement planning, capable of adapting to the vicissitudes of life without compromising the integrity of the retirement corpus.

Process of Annuity Purchase at Retirement

The journey towards retirement with the National Pension Scheme culminates in a crucial milestone: the purchase of an annuity. Upon reaching retirement, NPS subscribers are presented with the opportunity to convert a portion of their accumulated corpus into an annuity, essentially buying peace of mind and financial stability for the years ahead.

Subscribers must allocate a minimum of 40% of their total corpus towards buying an annuity, which then guarantees a steady income stream for life. The choice of the annuity provider is a decision of paramount importance, much like selecting a navigator for an uncharted journey. It involves comparing various annuity plans offered by different insurance companies empaneled with PFRDA (Pension Fund Regulatory and Development Authority), ensuring the provider’s reliability, service quality, and the annuity rates offered align with the subscriber’s expectations and financial needs.

Process Steps for Annuity Purchase at Retirement under NPS

The process below outlines the critical steps and options available for NPS subscribers approaching retirement, ensuring they can make informed decisions that align with their retirement goals and financial needs.

- Evaluate Annuity Providers: Research and compare various annuity plans offered by PFRDA-empaneled insurance companies.

- Determine Annuity Type: Decide on the type of annuity based on personal financial needs, such as fixed monthly payments or inflation-adjusted payments.

- Allocate Corpus: Allocate a minimum of 40% of the NPS corpus to purchase the annuity.

- Select Annuity Provider: Choose an annuity provider based on the stability, reliability, and annuity rates offered.

- Complete Documentation: Fill out the necessary forms and submit required documents to the chosen annuity provider.

- Purchase Annuity: Finalise the purchase of the annuity plan with the provider.

- Start Receiving Payments: Begin receiving pension payments as per the chosen annuity option.

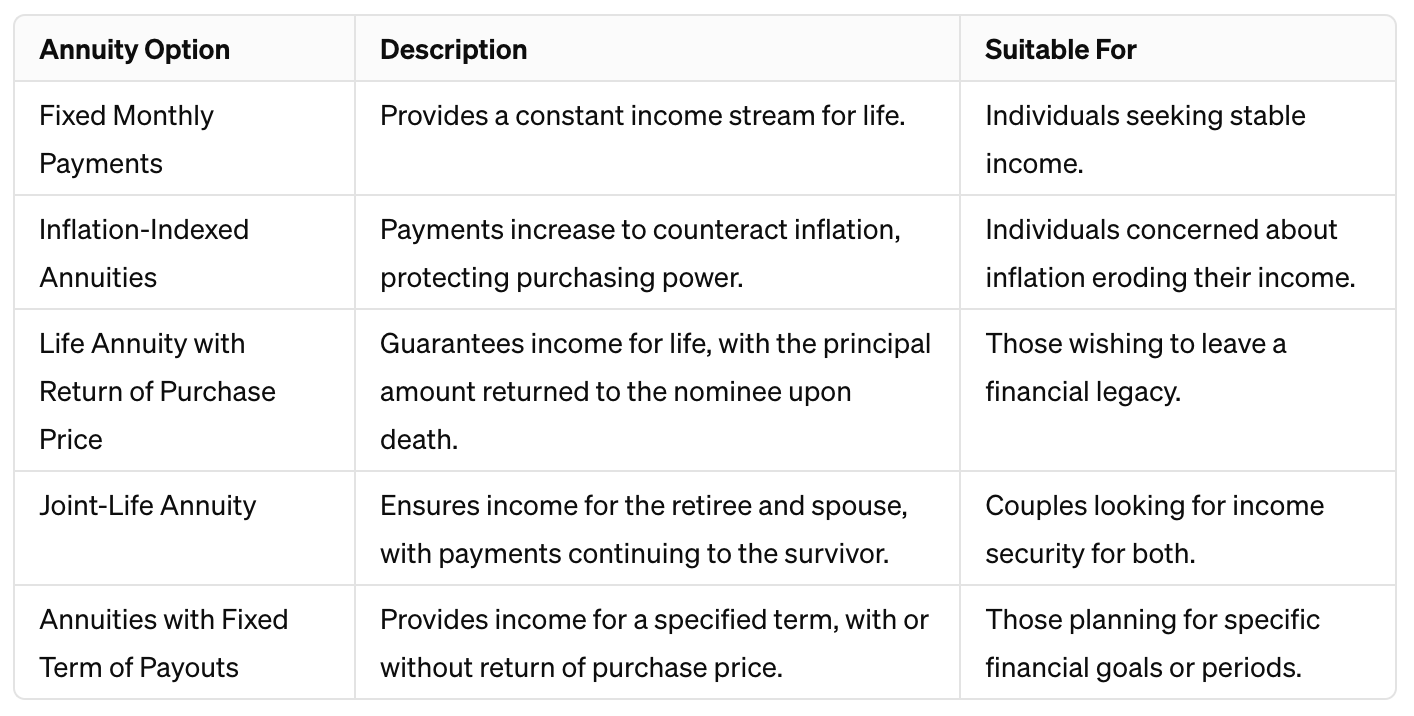

Options for Receiving Pension Payments

A wide range of pension payment options serves to cater to the multifaceted needs of India’s retirees, reflecting the rich tapestry of lifestyles and financial goals prevalent across the country. From fixed annuities that provide a consistent income stream to inflation-indexed annuities that offer increasing payments to counteract the eroding value of money over time, the choices are manifold.

Subscribers might opt for a life annuity with a return of purchase price to ensure that, upon their demise, the principal amount is returned to their nominee. Others might choose a joint-life annuity to ensure continuity of income for their spouse. The flexibility also extends to opting for annuities with or without a fixed term of payouts, catering to those who wish to plan for a defined period or seek lifetime security, respectively.

This strategic approach to selecting annuity plans enables retirees to sculpt their retirement income in a manner that best suits their life’s vision post-retirement—whether that involves ensuring a stable income for day-to-day expenses, providing for a spouse after one’s passing, or adjusting for the inflationary pressures that might erode purchasing power over time. The annuity purchase at retirement under the NPS is therefore more than a mere financial transaction; it is a critical step towards securing a financially independent and dignified retirement.

Comparing NPS with Direct Equity and Mutual Funds

When deliberating over the best avenues for long-term investments, Indian investors often weigh the merits of the National Pension Scheme against direct equity investments and mutual funds. Each option presents a unique blend of benefits, risks, and growth potentials. While the NPS is lauded for its structured approach to retirement savings, direct equity and mutual funds offer pathways to potentially higher growth and more flexibility, albeit with their own set of considerations.

Growth Potential

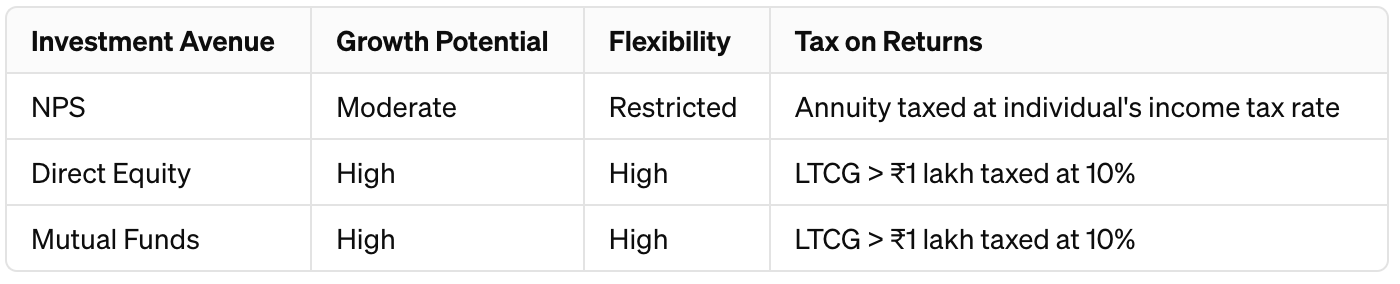

– NPS: Primarily designed as a retirement savings vehicle, NPS investments are spread across equities, corporate bonds, and government securities, with caps on equity exposure. This diversification aims to balance risk and return over the long term.

– Direct Equity and Mutual Funds: Offer the potential for higher returns, especially for well-chosen equity portfolios and mutual funds that have historically outperformed traditional retirement schemes. The absence of an upper limit on equity exposure allows investors to fully capitalise on the growth potential of the stock market.

Flexibility

– NPS: Comes with certain restrictions regarding withdrawal and compulsory annuitization of a portion of the corpus upon retirement.

– Direct Equity and Mutual Funds: Provide greater liquidity and flexibility. Investors can enter and exit positions as per their investment strategy without stringent restrictions.

Tax Considerations

One of the critical distinctions between NPS and other investment avenues lies in their tax treatment, especially concerning long-term capital gains (LTCG) and annuity income.

– NPS: While contributions and accumulations enjoy tax benefits, the annuity income received post-retirement is taxable at the individual’s applicable income tax rate. This could potentially lead to a higher tax outgo in the retirement years.

– Direct Equity and Mutual Funds: Long-term capital gains exceeding ₹1 lakh from equities and equity-oriented mutual funds are taxed at a flat rate of 10%, without the benefit of indexation. This more favourable tax treatment can significantly enhance the post-tax returns of these investments over the long term.

Illustrative Comparison Table

To visualise the differences, let’s consider an illustrative table based on hypothetical long-term investments in NPS, direct equities, and mutual funds:

This table underscores the potential for higher growth and more favourable tax treatment with direct equity and mutual funds, notwithstanding the disciplined savings and retirement focus offered by NPS.

While the NPS provides a structured approach to retirement savings with its inherent tax benefits, direct equities and mutual funds emerge as compelling alternatives for investors seeking higher growth and flexibility. The choice between these investment avenues should be informed by individual financial goals, risk tolerance, and tax considerations. A well-crafted portfolio, possibly incorporating elements of both NPS and direct market investments, could offer a balanced path to financial security and wealth accumulation. Investors are encouraged to consult with a SEBI Registered Investment Advisor to tailor an investment strategy that best aligns with their long-term objectives and financial situation.

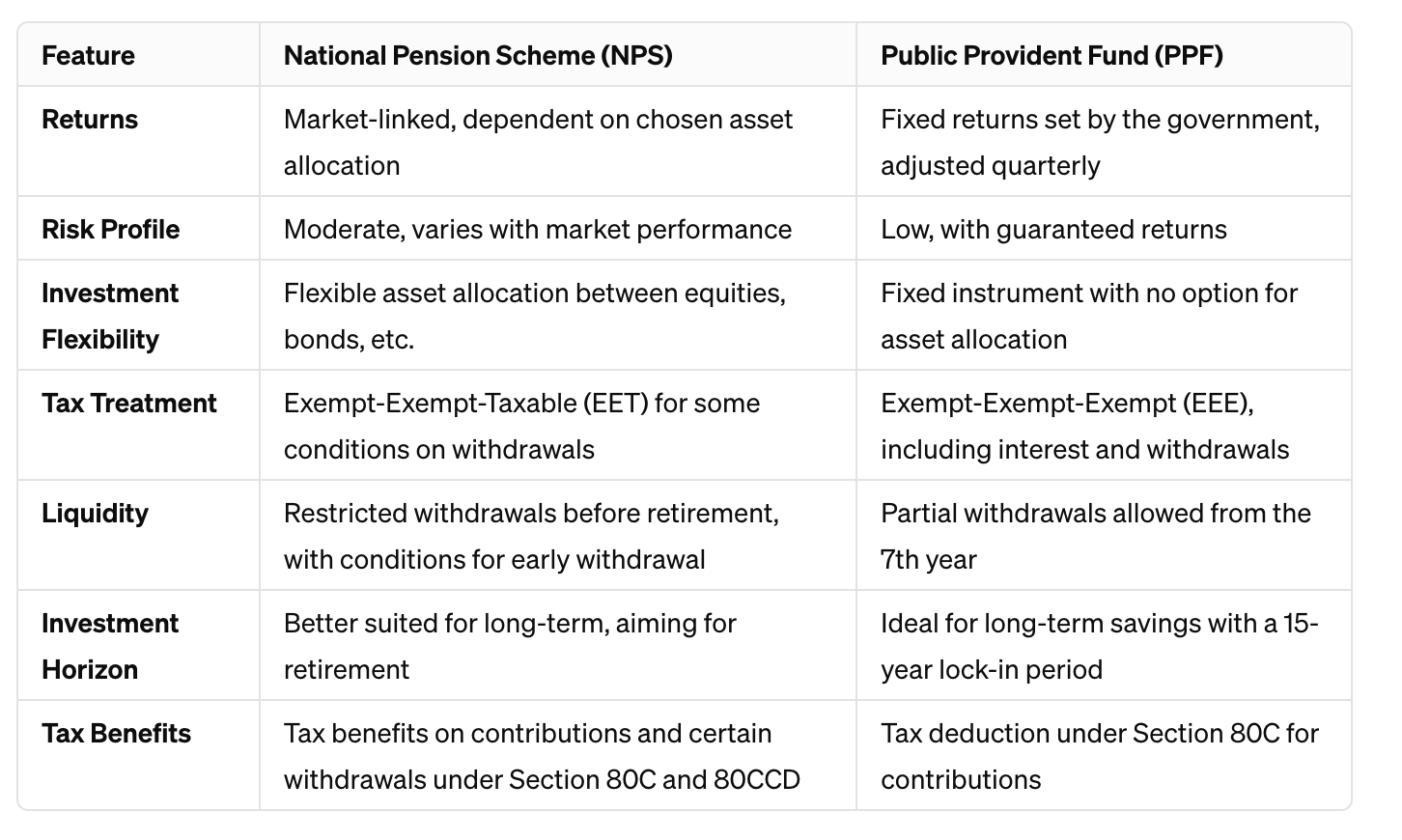

Comparing NPS with Other Retirement Planning Schemes

NPS and PPF represent two prominent festivals in this landscape, each with distinct features. NPS offers market-linked returns and the flexibility of asset allocation, suited for those seeking growth with a moderate risk appetite. PPF, on the other hand, is like a time-honoured tradition, offering guaranteed returns and safety, preferred by those with a conservative outlook towards savings.

NPS offers market-linked growth potential stands whereas PPF’s stands for safety and predictability. While NPS offers tax benefits on investments, returns, and withdrawals under certain conditions, PPF enjoys a tax-exempt status, making it a cornerstone of tax-saving strategies. The choice between the two hinges on individual financial goals, risk tolerance, and investment horizon, underscoring the importance of personalised financial advice.

This comparison highlights the key differences between the National Pension Scheme and the Public Provident Fund, guiding individuals in making an informed decision that aligns with their retirement planning goals. While NPS offers the potential for higher growth through market-linked investments and flexible asset allocation, PPF provides a safer, fixed-return avenue with comprehensive tax benefits. The choice between NPS and PPF depends on individual financial goals, risk tolerance, and the need for liquidity, underscoring the importance of tailored financial planning.

12. NPS for Different Sectors and Demographics

NPS holds out various options for an investor depending on where they work. The choice of how much and whether to invest in NPS is largely driven by this.

NPS for Government Employees

For government employees, the National Pension Scheme is a cornerstone of retirement planning. Initially tailored for this demographic, NPS offers a structured path to financial security post-retirement. Government employees benefit from a co-contribution system, where both the employee and the employer contribute to the NPS account, ensuring a substantial corpus upon retirement.

NPS for Private Sector Workers

In the private sector, NPS offers workers an optional avenue to secure their retirement. Acknowledging the diverse nature of private sector employment, from startups to conglomerates, NPS provides a flexible yet robust framework for retirement planning. Private sector workers are increasingly recognizing the value of NPS, drawn by its market-linked returns, tax benefits, and the flexibility to tailor their investment choices. This shift underscores a growing awareness of the importance of retirement planning across India’s corporate landscape.

NPS for Self-Employed Individuals and Informal Workers

The inclusion of self-employed individuals and informal sector workers under the NPS umbrella marks a significant milestone in India’s pension reform journey. Catering to a segment often overlooked by traditional pension schemes, NPS offers a semblance of security and stability in the unpredictable world of self-employment and informal labour. By enabling contributions as per one’s financial capacity, NPS democratises retirement planning, extending its benefits to carpenters and consultants alike, weaving a safety net that spans across India’s vast economic spectrum.

Conclusion

The National Pension Scheme stands as a lighthouse guiding Indians towards a secure retirement, offering a blend of growth potential and flexibility unmatched by traditional investment avenues. Its design, mirroring the diversity and resilience of India itself, offers a path to financial security for millions.

To sum up, the National Pension Scheme stands as a beacon for disciplined retirement planning in India, offering a structured pathway towards securing financial stability in one’s golden years. Through its dual-tier system, the NPS harmonises the principles of long-term savings with the flexibility to meet intermediate financial needs. With options spanning from conservative government bonds to more aggressive equity investments, the scheme caters to a diverse range of investor profiles and risk appetites.

While it presents a promising avenue for retirement savings, especially with its tax advantages, it’s crucial to recognize that alternatives like direct equity investments and mutual funds could provide higher growth potential and greater liquidity, albeit with different tax implications. The strategic juxtaposition of NPS with other investment vehicles, leveraging their unique strengths, could thus pave the way for a robust, diversified investment portfolio.

As we navigate through the various investment options available, it’s imperative to align our choices with our financial goals, risk tolerance, and retirement aspirations, possibly under the guidance of a trusted SEBI Registered Investment Advisor. The journey to financial security is multifaceted, and the NPS, with its structured approach to retirement savings, serves as a critical component of a holistic investment strategy aimed at fostering a financially secure and prosperous future.

Frequently Asked Questions about NPS

In addressing frequently asked questions about the National Pension Scheme, it’s crucial to dispel myths, clarify features, and spotlight the benefits of one of India’s most pivotal retirement savings mechanisms.

What is the National Pension Scheme?

NPS is a government-sponsored pension scheme in India, designed to provide subscribers with a long-term saving avenue to plan for retirement through safe and reasonable market-based returns. It’s structured around individual accounts known as Permanent Retirement Account Number (PRAN), offering both Tier I (non-withdrawable until retirement) and Tier II (voluntary and withdrawable) accounts.

Who can join the NPS?

Any Indian citizen between the ages of 18 and 65 can join NPS, making it a versatile option for early career professionals, mid-career individuals, and those nearing retirement. It’s inclusive, catering to both the organised and unorganised sectors, including self-employed professionals.

How does NPS work?

NPS operates on a defined contribution basis where the contributions accumulate over time depending on the chosen investment options. At retirement, subscribers can withdraw a portion of the corpus as a lump sum and use the remaining to purchase an annuity for a regular pension.

What investment choices does NPS offer?

NPS offers two approaches: Active Choice, allowing subscribers to tailor their asset allocation across equities, corporate bonds, government securities, and alternative investments, and Auto Choice, a lifecycle fund that automatically adjusts asset allocation based on the subscriber’s age.

Are there any tax benefits?

Yes, NPS subscribers enjoy tax benefits under Section 80C and Section 80CCD, including an additional deduction for investment up to ₹50,000 under Section 80CCD (1B), which is over and above the ₹1.5 lakh limit under Section 80C.

What is the difference between Tier I and Tier II accounts?

Tier I is a primary account mandatory for all subscribers, offering tax benefits but with restrictions on withdrawals. Tier II is a voluntary savings facility accessible only to Tier I account holders, offering greater flexibility in terms of withdrawal but without the tax advantages.

Can I switch from one investment option to another or change the fund manager?

Yes, NPS allows subscribers to change their investment option (from Active to Auto Choice and vice versa) and switch fund managers to suit their changing risk appetites and financial goals.

What happens to the NPS corpus if a subscriber dies before retirement?

In the event of a subscriber’s untimely demise, the entire accumulated corpus is paid to the nominee/legal heir of the subscriber, ensuring financial support to the subscriber’s family.

How are NPS withdrawals taxed?

As of the current tax laws, 40% of the corpus withdrawn at retirement is tax-exempt if used to purchase an annuity. The remaining 60% is tax-exempt if withdrawn as a lump sum. However, the tax treatment of annuity income is subject to income tax as per the subscriber’s tax slab.

What are the annuity options available at retirement?

NPS offers various annuity options through insurance companies, including life annuity with a return of purchase price, life annuity with increasing payout, joint life annuity, and more, allowing retirees to choose based on their financial needs and family obligations.

Can I open an NPS account online?

Yes, opening an NPS account has been made convenient through the eNPS platform, where individuals can register, contribute, and manage their accounts online, reflecting the scheme’s adaptability to the digital age.

How does NPS fit into my overall retirement planning?

NPS should be viewed as part of a broader retirement planning strategy, complementing other savings and investment avenues. Its low-cost structure, market-linked returns, and tax efficiency make it a compelling component of a diversified retirement portfolio.